Russia’s invasion of Ukraine has led to a dramatic shift in oil, gas and refined product trade flows, as well as billions of dollars in capital investments in limbo due to crippling sanctions. Russia contracts a lot of processing technologies and equipment from Western countries, with deals cancelled due to sanctions.

Many European countries have banned the import of Russian crude oil, gas and refined products. This has forced Russia to look elsewhere for energy trading partners, which it has found primarily with China and India. Russia has also increased diesel shipments to Central and South America—primarily to Brazil, Cuba, Panama and Uruguay—and fuel oil and vacuum gasoil to other countries, such as Malaysia, Saudi Arabia, Singapore, Turkey and the UAE.

Despite sanctions, Russia has vowed to continue investing in its energy value chain, including the modernisation of several refining units and increasing domestic petrochemicals production capacity, with a focus on mitigating carbon emissions from refining operations (e.g., Rosneft’s 2030 strategy). At the time of publication, Russia had only a few projects remaining from its $55b refining modernisation programme. The country has focused over the past several years on investments aimed at increasing secondary unit capacity to produce higher-grade fuels for export. The timetables for these projects have been delayed due to sanctions, however.

Eastern Europe & CIS

Several notable capital investments and initiatives are under development in Eastern Europe and the CIS:

- Albania: To align closer to EU initiatives, the Albanian government plans to increase the use of biofuels and renewable energy in the transportation sector.

- Azerbaijan: State-owned SOCAR is investing more than $1b to expand and modernise its Heydar Aliyev refinery. The project includes increasing the refinery’s crude processing flexibility, boosting the production of Euro-V fuels and optimising operational costs. Once completed, the refinery’s processing capacity will increase by 1.5mt/yr, to 7.5mt/yr, with catalytic cracking capacity increasing by 500,000t/yr, to 2.5mt/yr.

- Croatia: Croatian oil and gas company INA is investing approximately $685m to upgrade its Rijeka refinery. The project focuses on installing a new heavy residue processing unit. Once complete in mid-2024, the refinery will help mitigate fuel imports, especially for diesel.

- Georgia: A 4mt/yr refinery is being developed in Kulevi. The project, worth more than $1.2b, is scheduled to be completed in 2024. Once operational, it will produce Euro-V and Euro-VI fuels, as well as reduce the country’s fuel imports by 15–20%.

- Kazakhstan: Due to the increase in domestic refined product consumption, Canadian firm PetroKazakhstan plans to double the size of the Shymkent refinery to 12mt/yr. The additional processing capacity will enable the company to satisfy the increasing domestic demand for fuels.

- Lithuania: Polish firm Orlen Lietuva is expanding the Mazeikiai refinery to produce cleaner transportation fuels. The c.$200m project includes the installation of a heavy residue conversion unit and is scheduled to be completed by 2025.

- Poland: To diversify its products portfolio, Polish firm Grupa Lotos is investing more than $300m on a new hydrocracked base oils plant. The complex will produce high-value Group 2 and 3 base oils once operational in H1 2025.

- Romania: Domestic firm OMV Petrom is planning to boost SAF and HVO biofuels production in the country by 2030. As part of the initiative, the refiner plans to produce up to 450,000t/yr of SAF and HVO at the Petrobrazi refinery, with plans to increase SAF production even more in the future.

- Serbia: As part of its $455m business plan, Serbian oil and gas company Naftna Industrija Srbije (NIS) will invest in Phase 3 of the Pancevo refinery’s modernisation project. NIS plans to reconstruct the facility’s fluid catalytic cracking plant and add a new ethyl tert-butyl ether plant.

- Turkey: Turkish refiner Tupras plans to add a new Ecofining plant to its Izmir refinery. The plant will convert 8,300b/d of waste feeds/feedstocks to SAF, renewable diesel and other products. The new facility will help Tupras reduce its carbon footprint and meet regulatory compliance.

- Uzbekistan: State-owned Uzbekneftegaz is investing nearly $680m to modernise its Bukhara refinery to adhere to new domestic fuel specifications. The first two phases of the three-phase project have been completed. These stages focused on increasing the production of Euro-IV and Euro-V fuels. The last phase, scheduled to be completed in 2025, focuses on increasing production of light oil products.

Western Europe

Two major shifts have occurred, or are in the process of occurring, within Western Europe:

- The ban on Russian refined products and gas imports in the region—a direct result of the war in Ukraine.

- The region’s move to net zero, which is reducing future transportation fuel demand but is also leading to new capital investments in biofuels production capacity.

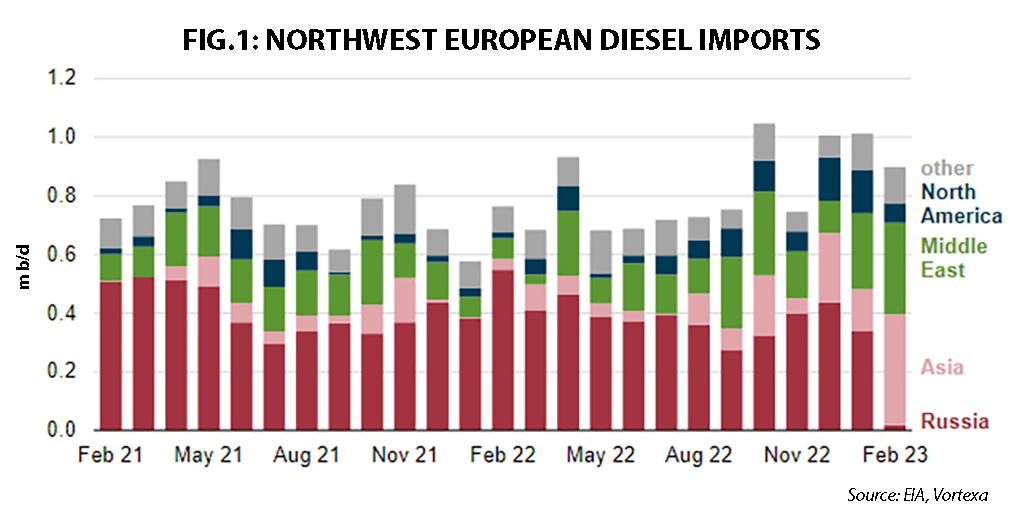

The EU has passed several bills restricting the flow of crude oil, refined products and gas from Russia since its invasion of Ukraine. A ban on Russian crude oil imports into the EU went into effect in December 2022 and was followed by a ban on Russian refined oil product imports, which took effect in early February 2023. Before the fuel/gas import ban, Russia supplied approximately 38% of crude oil and refined product imports into Europe. After the ban, Russian crude oil and refined product imports significantly declined from an average monthly figure of 15.2mt to 1.40mt, according to the European Commission. Refined product imports alone have dramatically decreased, falling from approximately 1.5m b/d to around 500,000b/d.

To help fill the void, Europe has increased crude oil and refined product imports from several regions, such as the Middle East (e.g., Saudi Arabia), China, South Korea, the US, West Africa and India, among others. For example, monthly diesel imports into the EU from Russia have fallen from a 53% market share to 2%, with regions such as Asia and the Middle East significantly increasing their shares (see Fig.1).

To adhere to provisions in the Paris Agreement, Western European nations are seeking pathways to mitigate carbon emissions and achieve net zero economies by mid-century. These plans include various ways of reducing carbon emissions, including the use of renewable energy and electrification, increasing the use of low-/zero-carbon hydrogen to power various industries, utilising low-/zero-carbon fuels for the region’s transportation (e.g., ‘Fit for 55’ initiative) and marine shipping sectors, increasing the use of biofuels and the possible future ban on the sale of diesel and gasoline-powered vehicles (the EU had planned to ban the use of internal combustion engines by 2035 EU countries such as Germany and Italy pushed back against this), among other initiatives.

In the hope of expediting the move to net zero, the EU revised the Renewable Energy Directive (RED) by increasing the bloc’s 2030 renewables target to 32%. The new version of the directive, RED 2, also includes a provision that targets fuel suppliers. RED 2 calls for a minimum of 14% of the energy consumed in road and rail transport to be renewable by 2030. This initiative also calls for the increased production of biofuels; however, RED 2 has also set limits on how EU nations can report their use of biofuels, bioliquids and biomass fuels.

The process of creating biofuels includes using land for farming to grow crops, which can possibly extend into other non-cropland areas to harvest other feedstocks (e.g., forests or wetlands)—a process known as indirect land-use-change (ILUC). This process can ultimately increase carbon emissions as it can cause the release of CO₂ stored within trees and soil. The EU believes that CO₂ released from ILUC could negate the greenhouse gas (GHG) emissions saved from increased biofuels usage; therefore, the EU has set limits on high ILUC-risk biofuels and other biofeedstock fuels. RED 2 also calls for growth in use of advanced biofuels, with their market share targeted to rise from 0.2% in 2022 to at least 1% in 2025 and up to 3.5% in 2030.

Due to the decline in transport fuel demand in the region, several refiners are adjusting their operations to process more bio-content feedstocks into biofuels. According to the European Federation for Transport and Environment, approximately 75% of the nearly $39b in spending by EU refiners to 2030 will go towards increasing biofuels production capacity. The EU’s biofuels production capacity could increase by 4mt/yr by 2030, while HVO production capacity could double to 10mt/yr within the same timeframe, the body says. The stark increase in HVO-produced fuels is a direct result of the maximum blend wall being reached in fatty acid methyl ester (FAME) production—FAME facilities produce biodiesel from lipids. HVO-produced fuels do not have a blend wall; however, the EU lacks the necessary feedstocks to fully realise its potential in this area, which means the region will have to import additional feedstocks. EU refiners are also investing in carbon-reduction technologies such as using green hydrogen for fired burners (a major source of refinery emissions) and other facility operations.

Several major European refiners are investing in new biofuels production capacity, including a stark increase in SAF production. At the time of publication, the EU had finalised SAF targets for airports. Fuel suppliers must ensure that SAF accounts for at least 2% of fuels supplied to EU airports by 2025, with this figure increasing to 6% by 2030, 20% in 2035 and up to 70% by 2050. This initiative is part of the EU’s ReFuelEU aviation rules, which fall under the Fit for 55 strategy.

Notable refining investments and initiatives in the EU are listed in Fig.2.

FIG.2: Notable refining projects/initiatives in Western Europe

This article is from a refining report which will look in more detail at Asia, the Middle East & Africa, Europe & Russia, and the Americas. To read the overview of the report, click here.

Comments