Two decades ago, Matthew Simmons published Twilight in the Desert, a critically acclaimed and well-researched book that wrongly warned of an oil shock and peak oil, claiming Saudi Arabia could not sustain production. Since then, there have been more false prophecies—including peak oil demand, countless OPEC obituaries and the saviour of US shale. But the truth is that Saudi Arabia and Middle East will likely be last oilmen standing.

While Petroleum Economist, OPEC and others have been screaming from the rafters about the lack of oil investment, the wider energy community only seems to take notice once the IEA wakes up to a fact. It is why IEA proclamations around peak oil demand are so dangerous—the agency has actively contributed to the lack of investment in oil and gas, stoking concerns over assets being left stranded given it takes a good 10–20 years, shale excluded, to go from exploration to production. It is a simple but unequivocal message lost in the age of transition and trilemmas: investors need returns.

The IEA’s somnambulism is indeed over. Its September report on oil and gas decline rates pointed out that nearly 90% of annual upstream oil and gas investment since 2019 has been dedicated to offsetting production declines rather than meeting demand growth. Investment in 2025 is set to be around $570b, and if this persists, modest production growth could continue in the future. And with oil demand growth set to persist given population growth, urbanisation, economic development and petrochemical and transportation requirements, that investment is as needed now as it ever was.

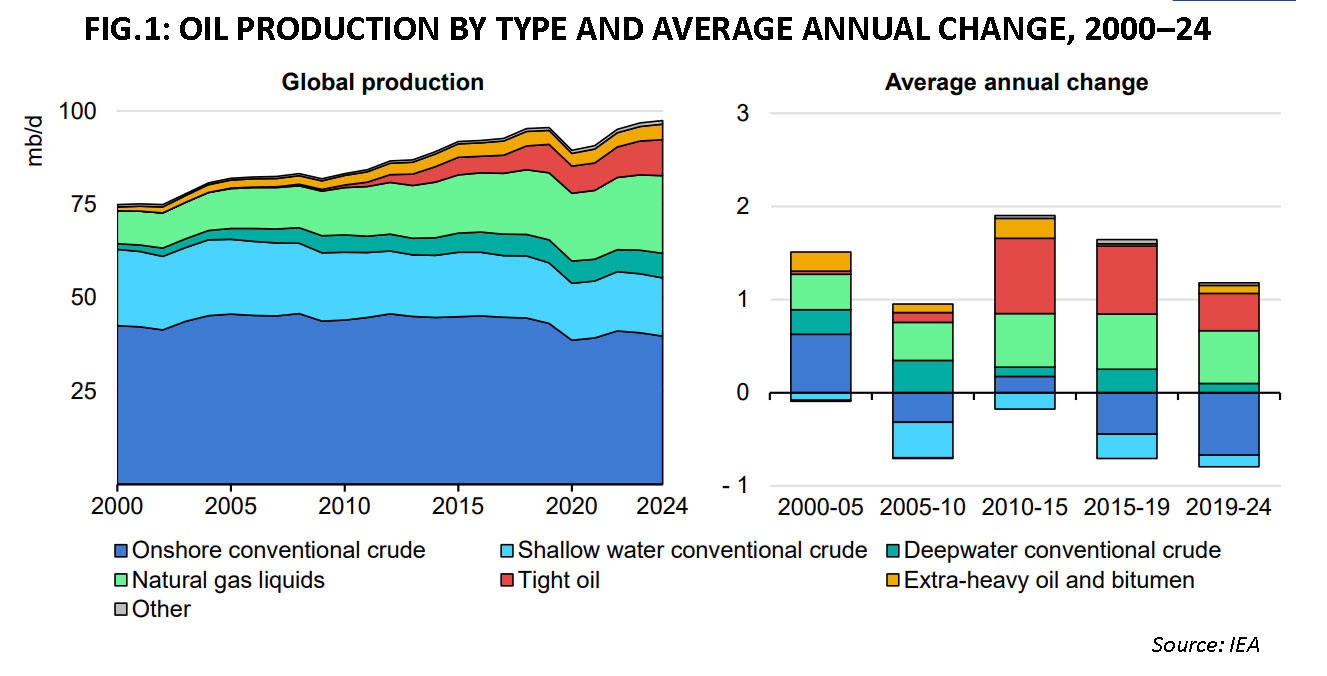

The rise of US shale oil and gas has been papering over the cracks. Conventional oilfields still make up 77% of total output and conventional gas fields comprise 70% of production, the IEA notes, with a heavy reliance on a small number of supergiant fields largely in the Middle East, Eurasia and North America. These accounted for around half of global hydrocarbons output last year.

And a closer inspection of the report reveals the Middle East, which holds the world’s largest conventional onshore fields, has the lowest observed post-peak decline rate, at 1.8%, while Europe, which has a very high share of offshore fields, exhibits the highest decline rate, at 9.7%.

And what is often forgotten is that oil and gas needs investment just to stand still. If all capital investment in existing sources of oil and gas production were to end immediately, global oil production would fall by 8% per year on average over the next decade, or around 5.5m b/d each year, according to the IEA. This is equivalent to losing more than the annual output of Brazil and Norway each year. Gas production would fall by an average of 9%, or 270bcm, each year, equivalent to total gas production from the whole of Africa today.

These are stark and pertinent analogies, not least because coinciding with the report was news of BP's discovery of a giant oilfield offshore Brazil. The Bumerangue find could hold more than 2b boe, with the oil major calling it the most significant in 25 years. It is hoped that this upstream positivity can lead to a greater wave of exploration that the IEA report belatedly cries out for.

The last boom years, 2010–14, are fading fast in the rear-view mirror, with the past ten years one of harsh exploration cuts, soul-searching, environmental criticisms and long-term demand doubts shaping the sector. And since the Guyana euphoria, there has been a slew of E&P disappointments with hopes around Namibia and the Orange Basin having been tempered along with failures in Norway and the East Mediterranean in 2025 and the hunt for the next Guyana still very much on.

Middle East shines, dusk elsewhere

The IEA also warns that natural decline rates are becoming steeper. In 2010, natural decline rates would have led to a 3.9m b/d annual drop in oil production and 180bcm annual drop in gas production. “The sharper natural decline rates observed now compared with 2010 reflects the higher reliance today on unconventional sources, changes in the mix of conventional production (such as more deep offshore fields and NGLs), and a higher supply base,” the report noted.

Most unconventional sources of oil and gas production generally exhibit much faster decline rates than conventional types. If all investment in tight oil and shale gas production were to stop immediately, production would decline by more than 35% within 12 months and by a further 15% in the year thereafter, the IEA highlighted.

Shale plays in the US are also becoming ‘gassier’, raising overall decline rates as oil-rich fields mature. Under natural decline rates, global oil and gas supply would become much more concentrated among a small number of countries in the Middle East plus Russia. Most oil production in the US comes from fast-declining unconventional sources, while in the Middle East and Russia most oil is produced from slowly declining conventional supergiant fields. Without further capital investment, rapid production declines—a 65% drop over the next decade— will dominate outside the Middle East and Russia, which would witness shallower drop offs of 45%, the IEA notes.

Hydrocarbon mathematics

If current levels of production are to be maintained, more than 45m b/d of oil and around 2tcm of gas would be needed in 2050. This can come from investment in existing fields to slow decline rates, from oil and gas projects that are still ramping up, from projects that have been approved and from ongoing investment in unconventional resources. Still, this leaves a large gap that would need to be filled by new conventional oil and gas projects to maintain production at current levels.

Around 230b bl of oil and 40tcm of gas resources have been discovered that have yet to be approved for development. The largest volumes are in the Middle East, Eurasia and Africa. Developing these resources could add around 28m b/d and 1.3tcm to the supply balance by 2050. Filling the remaining supply gap to maintain today’s production through to 2050 would require annual discoveries of 10b bl of oil and around 1tcm of gas. These amounts are just above what has been discovered annually in recent years. Developing these resources would add around 18m b/d and 650bcm of new oil and gas production by 2050.

There are other reasons why the Middle East is well positioned. The key OPEC members also produce a barrel of oil at the lowest cost and are dominated by NOCs that allow greater licence to invest when some international investors get cold feet. This changing global corporate profile offers a double-edged sword for oil and gas investment. Domestic NOCs have discovered 50% of commercial resource since 2020 and 63% in 2024, while large oil majors are gradually declining, with 50% fewer companies engaged in high impact exploration, according to consultancy Westwood Global.

And remember, oil and gas supply increasingly relies on fields with higher decline rates and complex operating environments, the interplay of investment decisions, economics and regulation will shape supply resilience and market stability. In other words, the energy climate needs to be conducive to investment otherwise the energy shock will be even greater, the costs to consumers higher and the security risk even more concerning.

The sun does not have to go down, but the investment horizon needs to change soon: policymakers, financiers and the wider energy community please take note before the darkness descends.

Comments