While questions grow over demand for transport fuel in the longer term, petrochemicals are likely to support crude demand and account for a bigger share of the overall oil product mix. Global ethane and naphtha demand are set to rise substantially over the next several years. These two feedstocks provide the basis for production of petrochemicals—primarily ethylene—which are then processed into further derivatives and products such as plastics.

Ethylene has broad application potential: both as a feedstock in the construction, packaging and transportation sectors and as a derivative including polyethylene and styrene. Polypropylene may also play a key role given its use in transport and electronics. Naphtha is also pervasive, with uses from paint and plastics to gasoline processing as well as the energy sector.

Asian surge

Global LPG/ethane and naphtha demand is forecast to increase by 1.7m b/d and 1.5m b/d, respectively, from 2022–28, according to the IEA. In fact, feedstocks for petrochemical production will account for approximately 40% of oil demand growth through the forecast period. In turn, several industry analysis reports show the global petrochemicals industry eclipsing $900b by the end of the decade. Petchems demand is a symptom of burgeoning population growth and urbanisation that puts Asia-Pacific as the leader and Europe—as a mature economy, as the laggard—in terms of additional appetite.

China’s capacity buildout includes several mega-refineries and integrated petrochemical complexes to meet the extra demand. India, meanwhile, has announced more than $140b in petrochemical grassroots and expansion projects to satisfy its booming demand. The slate of projects includes the country’s drive to create integrated plastics parks and chemicals clusters. By contrast, Europe is struggling amid a mature industry and high costs. However, the health of the petchems sector can be seen in even the slowpoke given that many countries in the region are still investing in new capacity. The IEA states that the petrochemical sector will remain the key driver of global oil demand growth—with LPG, ethane and naphtha accounting for more than 50% of the rise between 2022 and 2028 and nearly 90% of the increase compared with pre-pandemic levels.

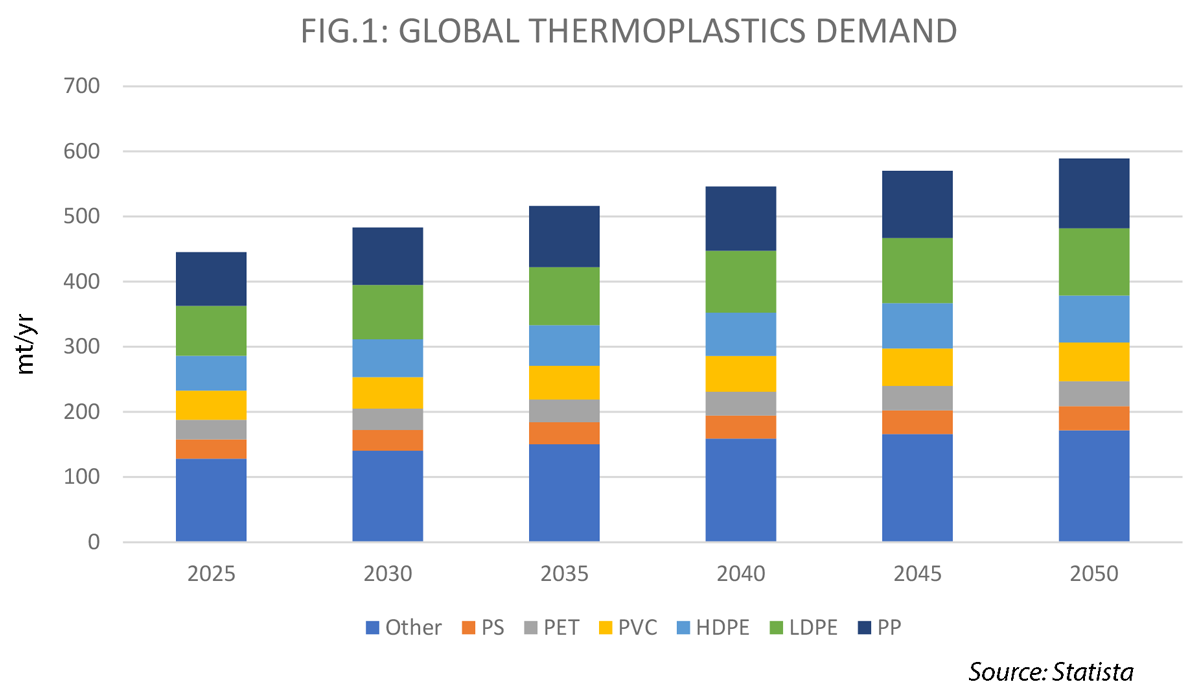

Global thermoplastic demand is expected to increase to 2050, amounting to nearly 590mt/yr (see Fig.1). Most of this increase is attributed to a stark increase in non-OECD Asia, primarily due to a surge in Asia’s middle class. In 2020, more than 3.5b people were considered part of the consumer class—i.e., those that spent around $12/d in 2017 purchasing power parity—according to thinktank the Brookings Institution and figures from data enterprise World Data Lab. Of these 3.5b people, half are in Asia, which is a significant increase since 2000, when 70% of the consumer class was in OECD countries—primarily in the West. By 2030, the size of the consumer class is forecast to increase to nearly 5b, with Asia comprising the bulk of the growth. This socioeconomic class has more purchasing power for many goods made with petrochemicals. The significant rise in Asian citizens entering the consumer class will be the driving force for petrochemicals through the rest of the decade.

Capacity needed

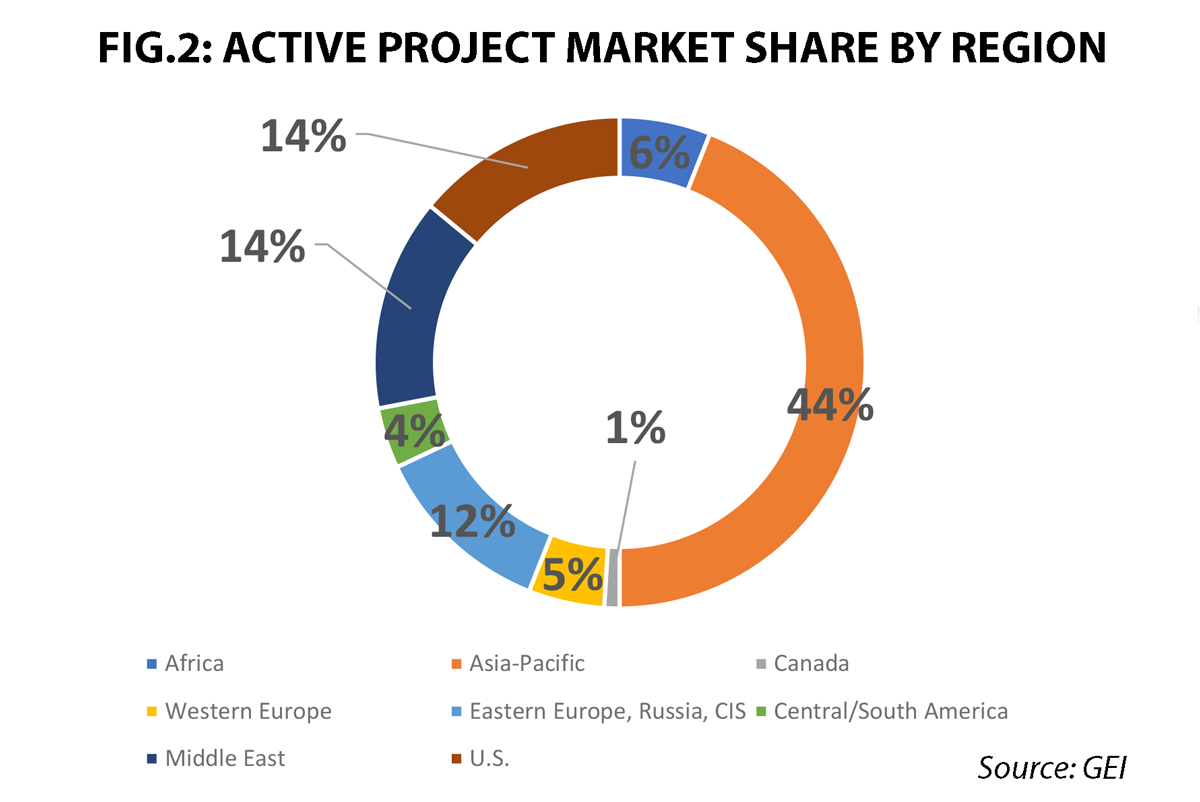

Additional processing capacity will be required globally to satisfy forecast demand for petrochemical products. More than 530 petchems projects are underway around the world, according to Gulf Energy Information’s Global Energy Infrastructure database. More than 40% of these are in the Asia-Pacific region, followed by the Middle East and the US. These three regions represent more than 70% of active petrochemical projects globally (see Fig.2).

When analysed by project status, 51% are in pre-construction phases, with the remaining 49% under construction. These projects represent more than $900b in petrochemicals capacity investment.

The upbeat assessment of petrochemicals is not without caveats, including worsening geopolitical risks, volatility in global oil markets and the threat of oversupply, which could depress both prices and spreads and lead to reduced investment and capped profits. Indeed, in 2023, global oversupply of petrochemicals is the highest in more than three decades. While this may partly relate to China’s stuttering demand, with the economic outlook in Asia and the rest of the world still misfiring, the overcapacity problem could well persist for some time to come.

This article is from a petchems report which will look in more detail at Asia, the Middle East & Africa, and Europe & the Americas.

Comments