The 27 EU members have slowly begun to cut imports of Russian diesel ahead of petroleum product sanctions set to come into force in February 2023. The shift has been some time coming.

In the six months following the initial invasion of Ukraine, EU27 seaborne gasoil/diesel arrivals sourced from Russia averaged 643,000bl/d, higher than the 585,000bl/d seen across the same period a year earlier. For some time, it seemed the EU’s need for gasoil/diesel outweighed the bitter distaste Russia’s illegal invasion had elicited on the continent.

But arrivals have since shown slow downward momentum. October imports finished at 546,000bl/d, above a September low of 510,000bl/d but well-off July’s 700,000bl/d. The coming months may see further downturns.

Europe certainly has a need for middle distillates—as evidenced by low sulphur gasoil crack spreads. Spot cracks are currently at just above $57/bl, more than $40/bl higher than a year ago. The market is clearly indicating a need for more barrels.

But the problem for European refiners is twofold. Firstly, hydrocracking margins have only recently returned to positive territory after months of sky-high hydrogen costs, owing to a gas price squeeze.

Hydrocracking is essential for a refinery trying to maximise diesel production. If gas prices spike again this winter, hydrocrackers will again become unprofitable to run and European refiners will face difficult decisions around how much diesel to produce, especially if optimisation requires heavy hydrocracker usage.

Secondly, EU member states’ crude import slates are growing ever lighter as firms restrict purchases of Russian crude—mostly Urals, which is particularly well-suited for diesel/gasoil output. Over the past eight months, EU27 seaborne Russian crude imports have quickly declined, down to just 1mn b/d in October, well off the 1.55mn bl/d 2021 average.

These barrels have been replaced, in part, by lighter, sweeter US grades, which tend to yield more light ends, including gasoline. EU27 oil imports from the US averaged 1.1mn bl/d in March–October, up by more than 300,000bl/d relative to 2021 as a whole. But sourcing grades with a similar API (c.30.6) to Russian grades is proving a more difficult task.

Seaborne imports of non-Russian oil with an API between 29 and 32 have managed only small gains. October’s arrivals averaged 586,000bl/d, just 40,000bl/d above the 2021 average.

The EU has several alternative, non-Russian sources from which to pull diesel/gasoil, including Saudi Arabia, the UAE and Kuwait of late. In October, combined imports from these three countries into the EU27 averaged 382,000bl/d, just under September’s year-to-date high of 400,000bl/d. Our expectation is that this trade flow has the potential to push higher as Russian sanctions approach.

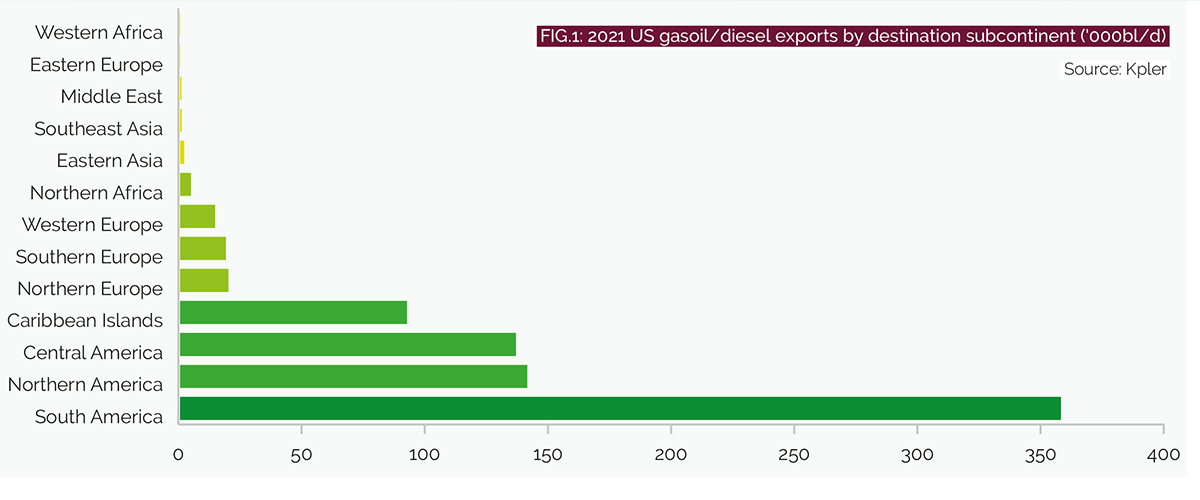

Only recently have US Gulf refiners shown a slight willingness to push more gasoil/diesel into Europe. In September, US departures for the EU pushed to 73,000bl/d, the highest in over a year. But Latin America remains US refiners’ central focus for now.

October’s US-sourced Latin American diesel/gasoil imports averaged 962,000bl/d, off August’s 1.13mn bl/d record high but well above the 710,000bl/d 2021 average. This is hardly surprising as the US has long been the region’s most important source of petroleum product deliveries.

But there is a distinct possibility US product flows will undergo a broader shift towards Europe in early 2023. Such prices might be dictated by not only post-Russian import ban prices but also economic manoeuvring among Latin American players. Brazil, in particular, has previously indicated a future ambition to lift large additional Russian diesel/gasoil volumes.

This would mark a major shift. However, year-to-date Brazil has imported almost no volumes from Russia, even after then Brazilian foreign minister Carlos Franca talked up Russian imports into the country’s agricultural and transport sectors during a July UN visit. And, following the Brazilian elections, it is possible the new Lula regime will be more averse to working with Russia.

Ultimately, Europe will find alternatives to Russian diesel: it has little choice. It appears unlikely the bloc will backtrack on previous sanctions commitments, meaning the period until February is likely to be bumpy as long-established trade flows are forced to readjust.

Winter will also play a role. If temperatures plummet on the continent, spot diesel price spikes are certainly possible. At this point, we expect outcomes ranging from relatively mild to catastrophic are all on the table for European diesel markets over the next several months.

Reid I’Anson is senior commodity analyst at the intelligence company, Kpler.

This article is part of our special Outlook 2023 report, which features predictions and expectations from the energy industry on key trends in the year ahead. Click here to read the full report.

Comments