Major trends in new US refining capacity are adhering to Tier 3 (clean fuel) regulations, processing the wave of lighter crudes produced by US shale plays (including the construction of grassroots processing facilities and debottlenecking projects), and increasing octane-boosting production capacity (e.g., alkylation and isomerisation). In total, the US is forecast to add between 540,000 bl/d and 600,000 bl/d of new distillation capacity, and more than 300,000 bl/d of secondary unit capacity by the early 2020s.

The US has begun to enforce its Tier 3 fuel regulations. The programme lowers sulphur content in gasoline from 30 parts per million (ppm) to 10 ppm. Large US refineries (those producing more than 75,000 bl/d) had to comply with the new standard at the start of 2017. Refiners producing less than 75,000 bl/d must adhere to the Tier 3 regulation by 2020. However, legal flexibilities allow refiners to adhere to this new regulation. Regardless, the nation's refiners are investing to upgrade their facilities to reduce sulphur content and improve energy efficiency.

At the time of this publication, Petroleum Economist's sister publication, Hydrocarbon Processing's Construction Boxscore Database was tracking nearly 50 active refining projects in the US. More than half of all active refining projects are in Petroleum Administration for Defense District (PADD) 3 (e.g., the USGC). Combined, PADDs 2 (Midwest US) and 3 represent 75pc of all active refining projects in the US. Nearly half of the active refining projects are under construction. A breakdown of active refining projects by activity level is provided:

- Engineering—10pc

- FEED—3pc

- Proposed/planning—41pc

- Under construction—46pc

Texas and Louisiana contain the largest number of active refining projects. These two states also contain the largest volume of refining capacity in the US—Texas has 29 refineries with a total installed capacity of 5.7mn bl/d, and Louisiana has 17 refineries with a total installed refining capacity of 3.3mn bl/d. These two states represent nearly half of the 18.6mn bl/d of total refining capacity in the US. According to the US Energy Information Administration's (EIA's) 2018 refining capacity report, the US has 135 refineries, with a total installed capacity of nearly 18.6mn bl/d. A breakdown on the number of refineries and processing capacity in each PADD is provided below:

- PADD 1 (East Coast)—8 refineries (1.2mn bl/d)

- PADD 2 (Midwest)—27 refineries (4.1mn bl/d)

- PADD 3 (USGC)—56 refineries (9.8mn bl/d)

- PADD 4 (Rocky Mountains)—15 refineries (683,000bl/d)

- PADD 5 (West Coast)—29 refineries (2.8mn bl/d)

Demand outlook

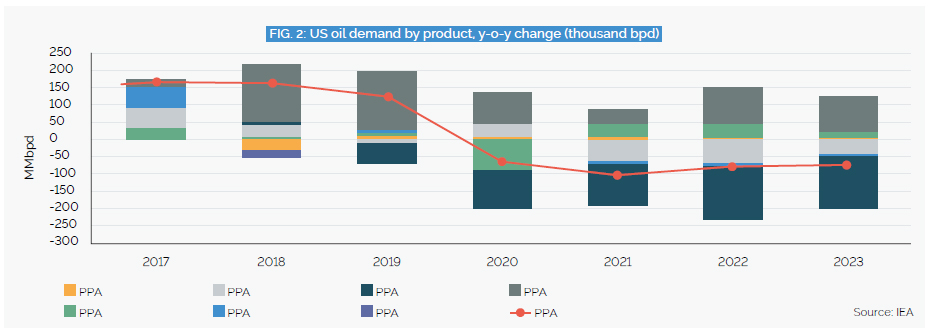

According to the US EIA, US crude oil consumption surpassed 19.8mn bl/d in 2017. Although consumption has increased, mainly on the back of low oil prices, domestic oil demand is forecast to increase to 2020, and then decline slightly into the early 2020s (Fig. 1). The increase, and subsequent decrease, in domestic oil demand will offset each other, and total demand remains virtually unchanged in the forecast period (2018–23). A y-o-y trend analysis on US oil demand by product is shown in Fig. 2.

The forecast decline in transportation fuels, such as gasoline, is primarily due to the increase in better-mileage vehicles, as well as the increased use of electric vehicles and hybrid electric vehicles. Despite the slight forecast decrease in fuels demand from 2020–23, at present, US refiners are processing more crude oil than ever before. From January 2017–August 2018, US refinery utilisation rates have averaged more than 91pc. The high utilisation rates have enabled US refiners to produce an average of more than 17mn bl/d of refined product output in 2018, reaching a record 18.2mn bl/d in August 2018.

Exports to rise

The surge in fuels production has allowed the US to not only meet increasing domestic demand, but it has also allowed the nation to boost exports. According to the US EIA, distillate fuel oil was the most exported petroleum product in 2017. Distillate fuel exports averaged 1.3mn bl/d in 2018, with the majority going to Central and South American countries. Over the past several years, most refined fuels exports from the US have landed in Latin America. For example, approximately 75pc of US distillate exports (e.g., 975,000bl/d) went to Central and South America. The percentage of gasoline exports from the US to Latin America is even greater. In 2018, out of more than 900,000bl/d of US gasoline exports, approximately 90pc landed in Latin America, with the majority—more than 500,000bl/d—heading to Mexico.

Many Latin American countries are still feeling the effects of the drop in low oil prices, which resulted in their inability to make necessary improvements and/or additions to domestic processing capacity to satisfy increasing demand. In the short term, Latin American countries would rather import refined fuels and petrochemical products than invest in capital-intensive capacity additions.

According to data from the US EIA, US refined product exports have increased from nearly 3.14mn bl/d in 2012 to 5.23mn bl/d in 2017. Approximately 52pc of refined product exports—nearly 2.7mn bl/d—went to Latin American countries in 2017. In that year, the top 15 destinations for US refined products accounted for nearly 3.9mn bl/d. These 15 nations accounted for 74pc of all US refined product exports. Out of these 15 nations, more than 2.14mn bl/d of US refined product was exported to Latin American countries.

It is likely that US fuel exports will continue to increase in the near term. Due to the complexity of the nation's refining system, the US is also in a great position to supply low-sulphur marine fuels that meet coming International Maritime Organization sulphur regulations. Many US refiners contain the necessary secondary units to produce the future fuels required by the global shipping industry.

Lee Nichols is Editor/Associate Publisher, Hydrocarbon Processing

Comments