Although the new Trump administration is likely to reduce regulation around drilling and oil production, US oil output nonetheless already hit record levels in 2024. October saw the figure reach 20.7m b/d—a new high for the monthly average.

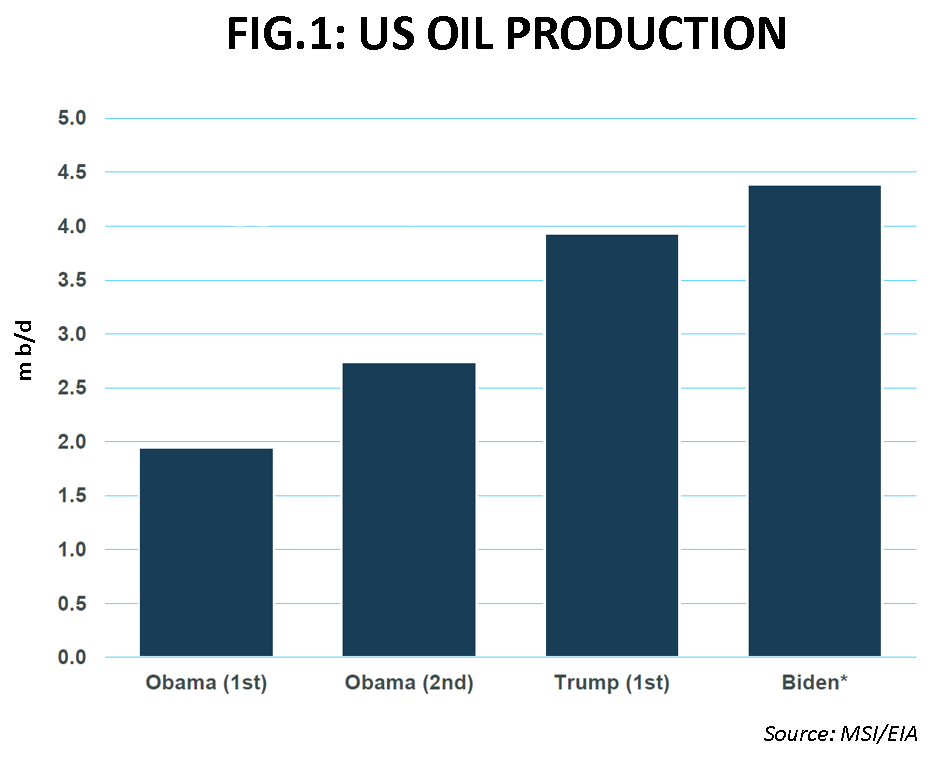

For comparison, when Donald Trump was first sworn in, in January 2017, US oil production was 12.3m b/d, increasing to 16.2m b/d by his last full month in office in December 2020. This of course included a major hit from Covid-19—US oil production in his first term peaked at 18m b/d in November 2019.

During the Biden administration, production has regained and exceeded these highs, adding what will be close to 4.5m b/d, once the president’s term is formally concluded (see Fig.1).

This is the most witnessed during any single presidential term and provides evidence to demonstrate that the Biden presidency cannot be defined as trying to suppress oil production, any more than the Trump presidency could be seen as proactively supporting it.

MSI therefore views the political rhetoric around the subject—and to some degree the Trump policies regarding the reregulation of drilling licences—as less important than the commercial decisions and investments which have actually driven output. One slogan prominent in the Trump campaign was ‘drill baby, drill’. The upstream president of the largest US oil company, ExxonMobil, said in late November that “We are not going to see anybody in ‘drill, baby, drill’ mode”, citing companies focusing on cost discipline and production economics.

Moreover, one area where the oil industry has concerns, from a cost perspective, is the impact of potential tariffs on supply chains. This may prove the more influential, if not direct, component of Trump’s policy suite on oil production, rather than, for example, the paring back of methane emissions charges on oil and gas production—part of one of the signature policies of the Biden administration, the Inflation Reduction Act (IRA). Trump’s agenda may prove, unintentionally, restrictive on US production if it hits costs.

In the Trump transition, wider environmental regulation and policy initiatives implemented under Biden with regard to oil use are also likely to be rolled back. However, given the prominent backing for Trump given by Elon Musk, changes in the support for electric vehicle sales provided during the Biden term by the IRA could be more nuanced. Tesla’s market share of light electric vehicles (EVs) in the US is close to 50%.

One key policy that has been flagged by Trump is the $7,500 consumer tax credit for EV purchases. EV sales in the US hit 9% of total car sales in Q3, their highest proportion yet, though still well below China. Should tax incentives be removed, manufacturers will be forced to reduce prices to drive sales.

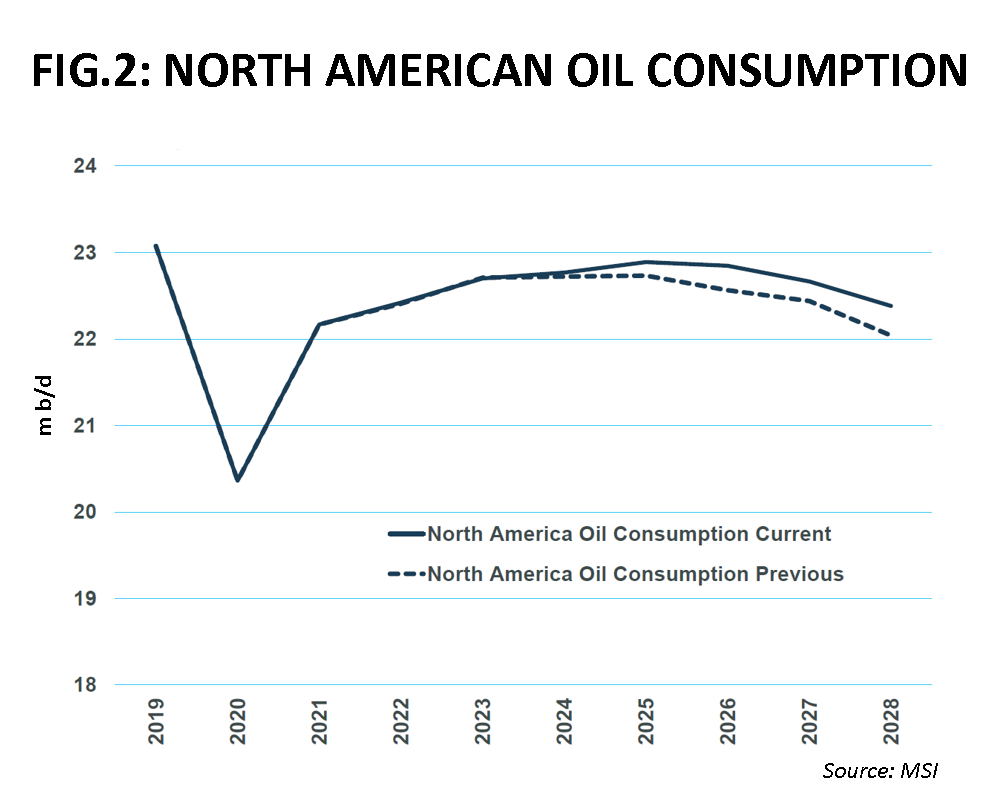

For consumers, the direct benefits of EVs appear increasingly questionable. A widely quoted study by McKinsey of US motorists saw 29% of EV owners considering a switch back to internal combustion engine vehicles. The main reasons for this view were concerns around the lack of charging infrastructure, cost of ownership and range limitations. Continuing consumer momentum towards EVs appears to be a harder sell and supports an increase in long-term North American oil consumption versus our previous outlook (see Fig.2).

Crude exports

Along with oil production, US crude exports have also broken new ground this year, averaging 4.1m b/d in the first three quarters of 2024.

US crude exports flow in a fairly even distribution to Europe and Asia, with the latter destination driving higher tonne-miles. For Europe, additional US supplies have been a key substitute for lost Russian crude imports since the invasion of Ukraine.

Trade wars, primarily with China, were a major feature of Trump’s first term and look set to become a key part of his second. Trump explicitly targeted China, Mexico and Canada in late November, saying he will impose a 25% tariff on goods coming in from the two American neighbours as soon as he is inaugurated on 20 January 2025.

He also stated that “we will be charging China an additional 10% tariff, above any additional tariffs”. Along with oil production, US crude exports have broken new ground this year, averaging 4.1m b/d in the first three quarters of 2024. US crude exports to China typically fluctuate in the 200,000–300,000b/d range. This is a sizeable but not ‘game-changing’ volume for the crude tanker market, should China decide to retaliate on these measures.

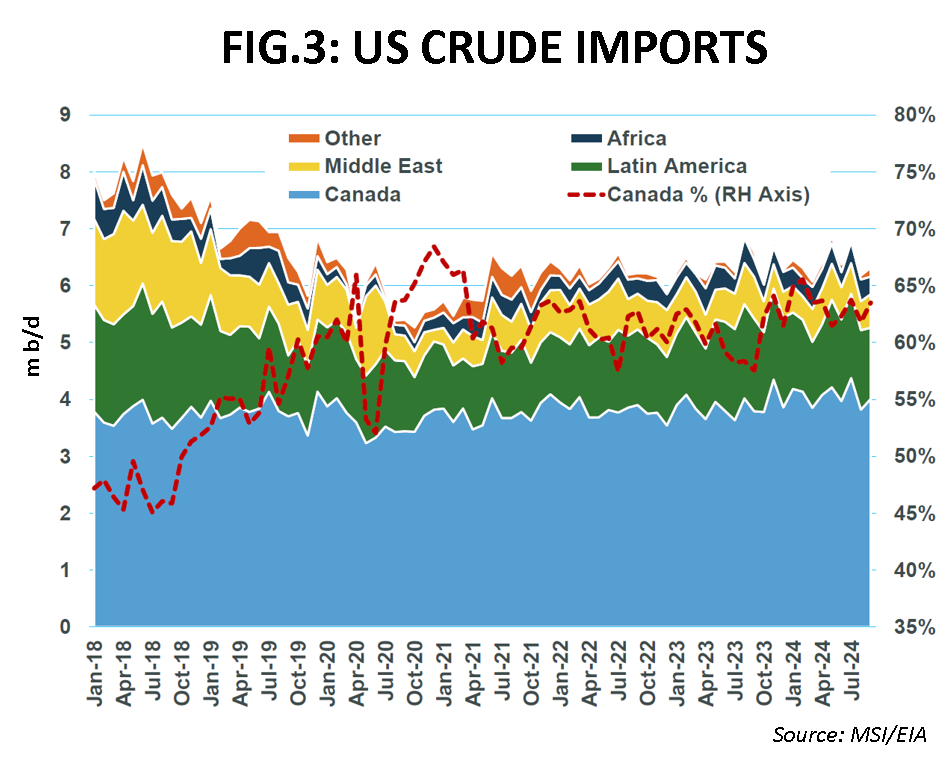

The tariffs on Canada and Mexico pose more of an issue for wider oil markets. Primarily this is because the US still imports more crude than it exports—about 6.0–6.5m b/d (see Fig.3). A large proportion comes from Canada, with Latin America and the Middle East also substantial contributors. Canada is by far the largest supplier, however, exporting about 4m b/d to the US, mainly via pipeline. More recently, additional seaborne volumes have entered the US west coast from Canada’s Transmountain pipeline.

Mexico is also a big trade partner, exporting about 500,000b/d to the US, mainly via seaborne shipments across the Gulf of Mexico—a major Aframax market. Therefore, given these volumes, at a price of $70/bl, for example, US refiners would spend about $115b/yr on Canadian and Mexican crude imports alone.

Under Trump’s tariffs, and with no change in the oil price, this import bill would increase to $144b. This will therefore increase the cost of oil imports and pump prices in the US, assuming refiners pass on the costs to consumers. In turn this could affect US oil demand negatively, or drive refiners to source imports from elsewhere. However, for the landlocked states dependent on Canadian imports in the Midwest/Rockies regions for example, they will not have a choice.

As with production then, the key impact of Trump’s agenda on oil demand may come more from knock-on costs associated with tariffs, than policies affecting EVs, which would at any rate take time to have a major impact on the market.

Trump policy is, however, likely to increase sanctions on Iran, with a reportedly ‘maximum pressure’ plan. This could prove increasingly problematic for Iranian crude exports to China which, according to Vortexa, buys an estimated 1.4m b/d, bypassing Western finance and sanctions via elaborate and shadowy supply chains.

Tim Smith is director of Maritime Strategies International.

Comments