The energy market is undergoing a deep transformation, not just technological or regulatory, but structural and systemic, with new interactions forming across value chains, sectors and regions, reshaping how global energy systems operate.

These evolving market dynamics increase the nation states’ and the regional and international trade’s exposure to shocks: geopolitical, environmental and economic. There is a rising level of uncertainty brought on by the pace and complexity of change, introducing a heightened unpredictability in energy supply, demand and policy outcomes.

We cannot speak about a true decarbonisation of the global energy system without acknowledging the vital role played by gas storage, which is far more than a technical asset—it is a strategic pillar of the future energy system.

Currently, the global total working gas volume amounts to 424bcm, distributed across 699 storage facilities worldwide, with a withdrawal rate of approximately 7,371mcm/d. The vast majority of these storage facilities are developed in depleted natural gas fields.

North America enjoys the highest gas storage capacity—164bcm—followed by, at the opposite end, Latin America, with only 0.2bcm. Unsurprisingly, significant regional differences in the development of underground gas storage (UGS) largely reflect the development maturity of those regions’ gas infrastructure which, in turn, is closely linked to the evolution of gas demand.

In developed markets, UGS appears to be stagnating or experiencing only modest growth. These trends reflect differences in regulatory frameworks, market structures, geological possibilities and the integration of new gas developments, underscoring the ongoing need to adapt UGS strategies to evolving energy markets (national, regional and international).

The impact of UGS spans reliability, affordability and resilience as it ensures that large volumes of gas are available near demand centres, mitigating disruptions from technical failures, geopolitical tensions and extreme weather, while also playing a critical role during seasonal peaks and emergencies. While gas storage is not the only tool for achieving security of supply, it remains the most reliable solution and plays a key role in ensuring energy availability and reliability.

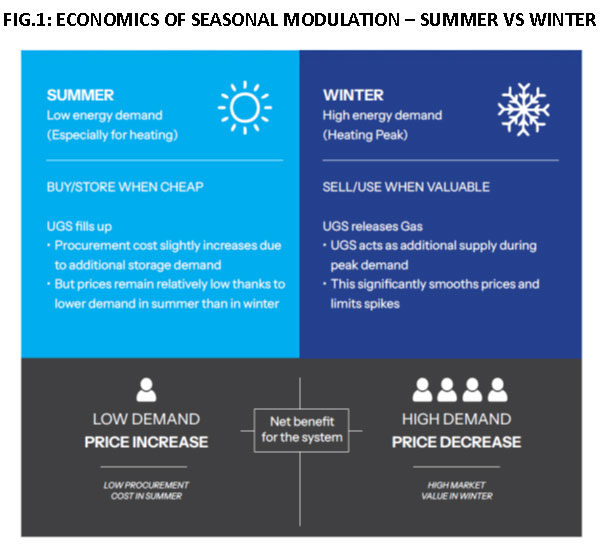

In mature gas markets, the sizing of storage capacities has been carried out by optimising the entire gas system to meet winter peaks during extreme cold weather. It is therefore possible to assert, based on the scenario developed by planning and competent authorities, that there is no substitute for underground storage to mitigate the actual energy needs during these extreme events.

Protection from extremes

By absorbing supply shocks and enabling price arbitrage, UGS protects consumers from winter/extreme heat price spikes and reduces the overall system costs. High storage levels have proven essential in stabilising markets during LNG price surges.

Acting as a buffer that enhances grid flexibility, it also lowers system costs by reducing the need for over-investment in transmission infrastructure. Most importantly, it prevents fallback to coal during supply stress and supports renewable integration without compromising the system’s reliability, and is thus a key enabler of decarbonisation.

Like carbon pricing, the strategic value of UGS must be internalised in energy systems’ design. It is not just a flexibility tool, it’s a cornerstone of resilient, affordable and clean energy frameworks.

While storage may seem less critical during periods of abundant supply, it remains vital as an arbitrage tool for ensuring energy provision at minimal costs to consumers, thereby underpinning prosperous economies. In competitive markets where reliability is assured, the true value of gas storage may be overlooked, especially in environments of ample supply. This oversight could lead to challenges if storage capacity, lacking regulatory support, becomes economically unviable, ultimately jeopardising the provision of consistent long-term services, particularly during unexpected events.

Overall, the ‘insurance value’ of UGS lies in its ability to provide a reliable, flexible and resilient energy infrastructure over the long term, one that can adapt to changing market

conditions, mitigate risks and support the transition to a more sustainable energy future. This is particularly valid for countries that had a strong dependence on gas suppliers or for countries where long-distance import gas pipelines were built.

While all gas assets across the energy system contribute to mitigating energy crises, UGS plays the most critical role in the face of unexpected events, demonstrating that—at present—no viable substitute exists for this asset.

As the power mix shifts increasingly towards renewables, the electricity grid becomes more exposed to volatility and requires structural adaptation. In this context, the need for long-duration energy storage becomes essential to ensure firm capacity and maintain grid reliability.

This shift calls for an end to siloed thinking, where sectors operate independently and market designs are tailored only to the fundamentals of their respective domains (gas or electricity). Instead, a more integrated, system-wide approach is required to reflect the interdependencies of a decarbonising and increasingly interconnected energy landscape.

Menelaos Ydreos is secretary general of the IGU. This article is taken from our Outlook 2026 report. To read Outlook 2026 in full, click here.

Comments