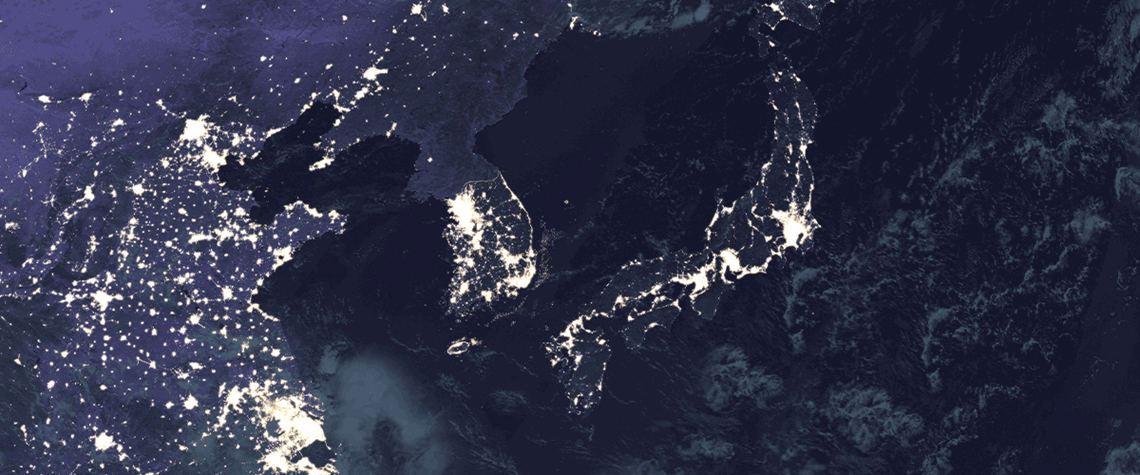

China is set to lead gas demand growth in Northeast Asia this winter

Muted winter LNG outlook for NE Asia

Seasonal temperatures will prove critical, but the LNG demand prospects for China, Japan and South Korea are currently soft

China is set to lead gas demand growth in Northeast Asia this winter amid signs the region’s biggest economy is bottoming out, although this is unlikely to mean a big jump in LNG imports as the country taps other sources of supply. And at the same time, more nuclear availability is expected to weigh on seasonal demand in Japan and South Korea. Recent green shoots in China’s economy suggest growth is stabilising, which may help domestic gas demand maintain momentum. China’s GDP beat predictions in Q3, with year-on-year growth of 4.9%, lifting growth for the first nine months of 2023 to 5.2%—ahead of Beijing’s official target of c.5%. Chinese gas demand has been strengthening since the spring,

Also in this section

1 April 2026

Golden Pass’s startup offers QatarEnergy a timely boost but may also force a difficult choice between honouring disrupted contracts and capitalising on soaring spot LNG prices

1 April 2026

It is not a case of if or when, but the length and magnitude of economic damage from elevated oil prices

1 April 2026

The US-Iran conflict demonstrates the need for diversification in several senses of the word. It also exposes the limits of Washington applying pressure on major oil and gas producers it considers geopolitical adversaries

31 March 2026

Disappointing results in its bidding round are a reality check for Libya, and global exploration generally