The oil market is witnessing one of the most dramatic conflicts in the Middle East in decades, raising the possibility of a prolonged disruption to the Strait of Hormuz—the most critical chokepoint in the global oil trade.

Processing facilities, refineries, ports and ships have already been damaged or destroyed. Tanker movements outside the Gulf have slowed sharply, forcing some producers to shut in production as storage fills. With no clear end to the conflict in sight, the physical oil market is tightening rapidly.

Yet the futures market appears almost calm by comparison. Brent has traded well above $100/bl, but many observers argue prices still fail to reflect the scale of potential shortages. The reason lies in the messy mechanics of the physical market: soaring premiums for prompt crude and shipping costs that have risen dramatically in a matter of days.

Futures markets versus physical reality

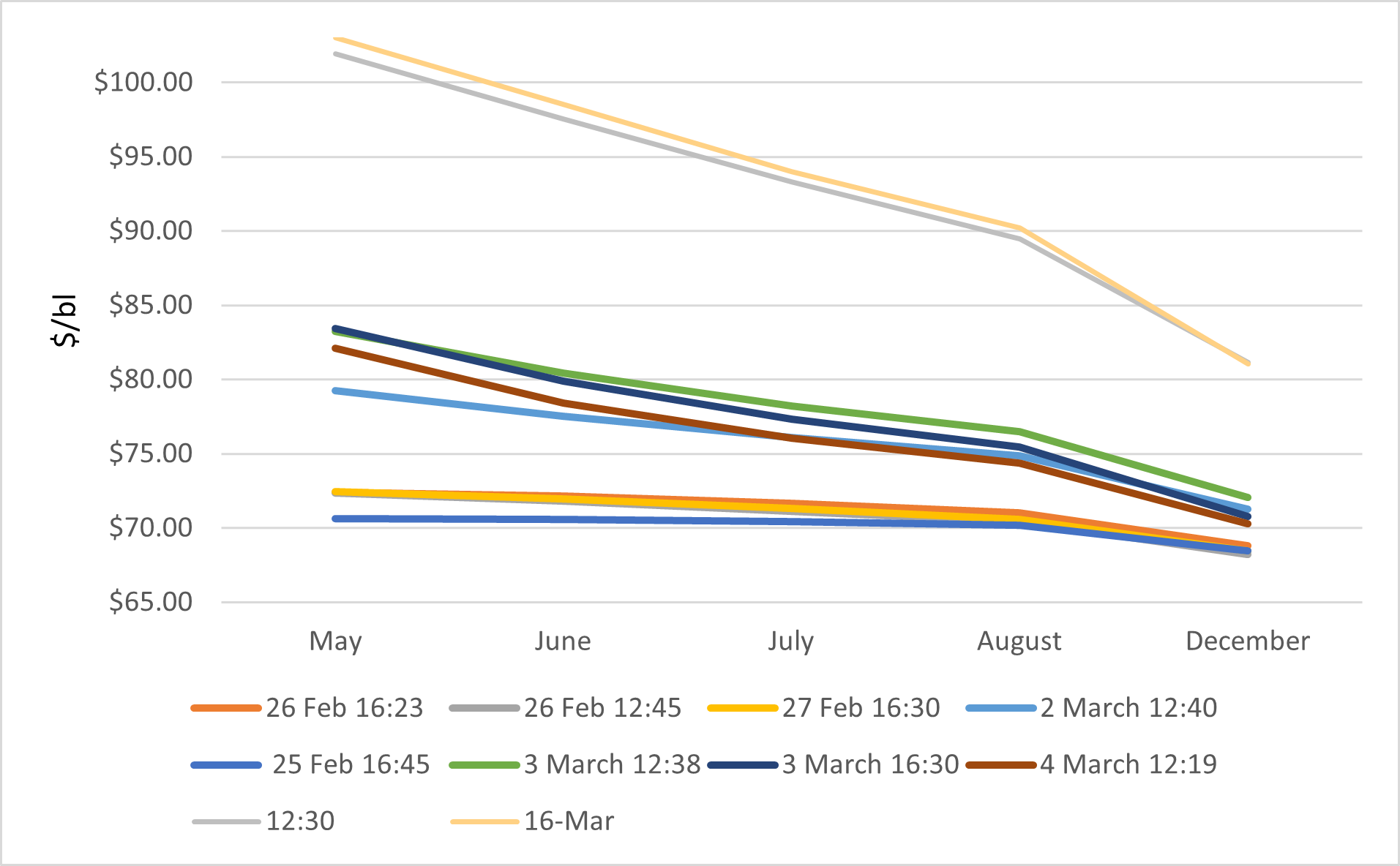

At the outset of the conflict, Brent barely reached the mid-$80s/bl. This surprised many observers, who expected an immediate move well above $100/bl. Even more striking, longer-dated contracts such as January 2027 Brent barely moved above $70/bl.

Clearly, the market had anticipated some form of geopolitical tension and priced it in. Traders initially expected something closer to a temporary disruption—perhaps comparable to the Venezuelan crisis, followed by a relatively swift return of exports.

As the geopolitical situation deteriorated, however, the front of the futures curve reacted strongly, while the back end remained anchored just above $70/bl (see Fig.1).

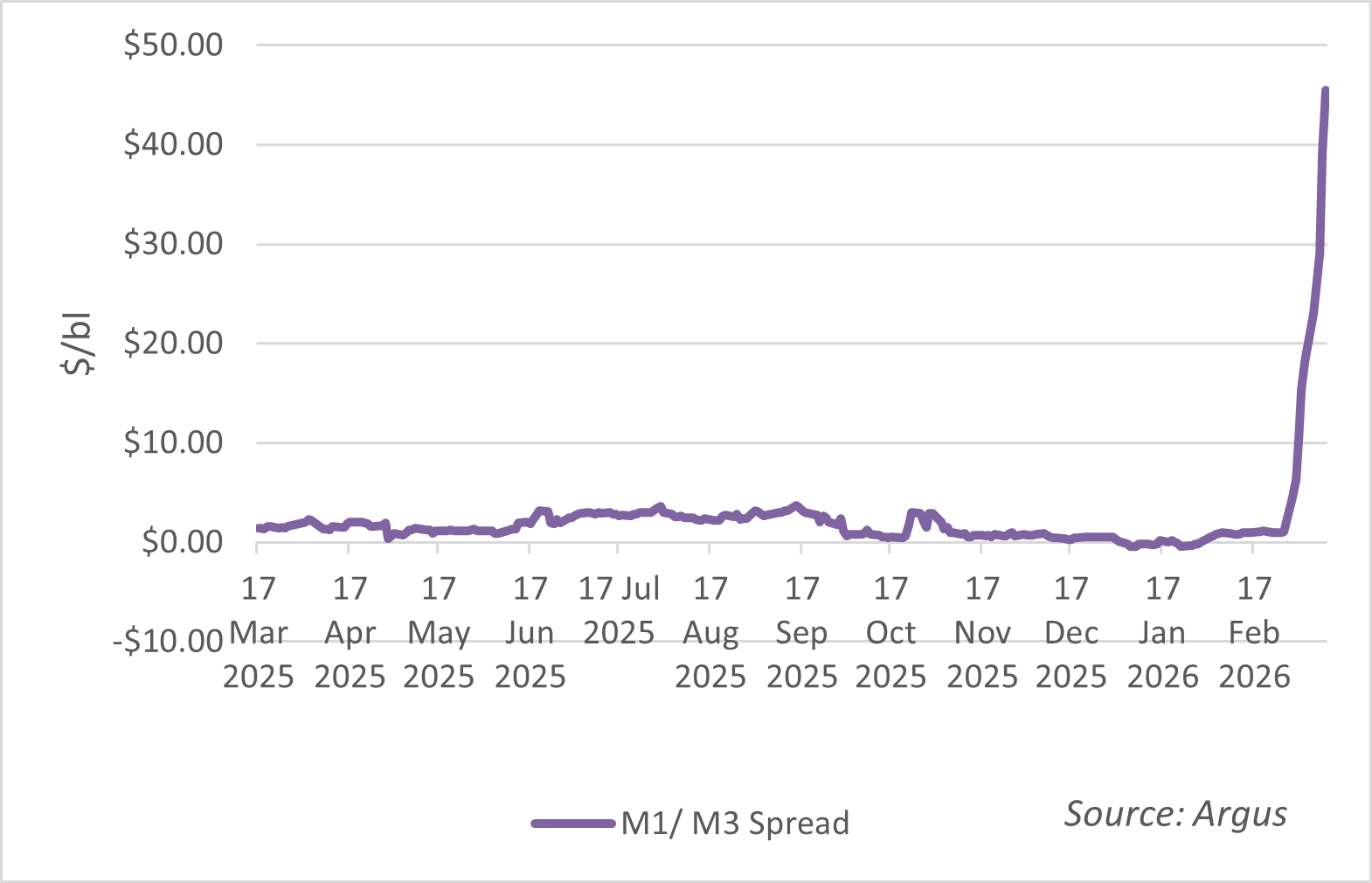

This divergence reflects a fundamental feature of oil futures markets: they are not designed to capture the full impact of immediate physical shortages. Benchmarks such as GME Oman or IFAD Murban currently trade May as the prompt futures month. But the real disruption concerns cargoes loading now—in March and likely April.

However, the premiums for those prompt barrels have surged toward $50/bl (see Fig.2). For refiners seeking immediate supply, the effective price of crude is therefore far higher than the futures curve suggests.

On 16 March, for example, Oman GME futures settled at $147.79/bl for May delivery. Add the premium for prompt physical barrels and the free-on-board price of Middle Eastern crude rises well above $150/bl.

The freight shock

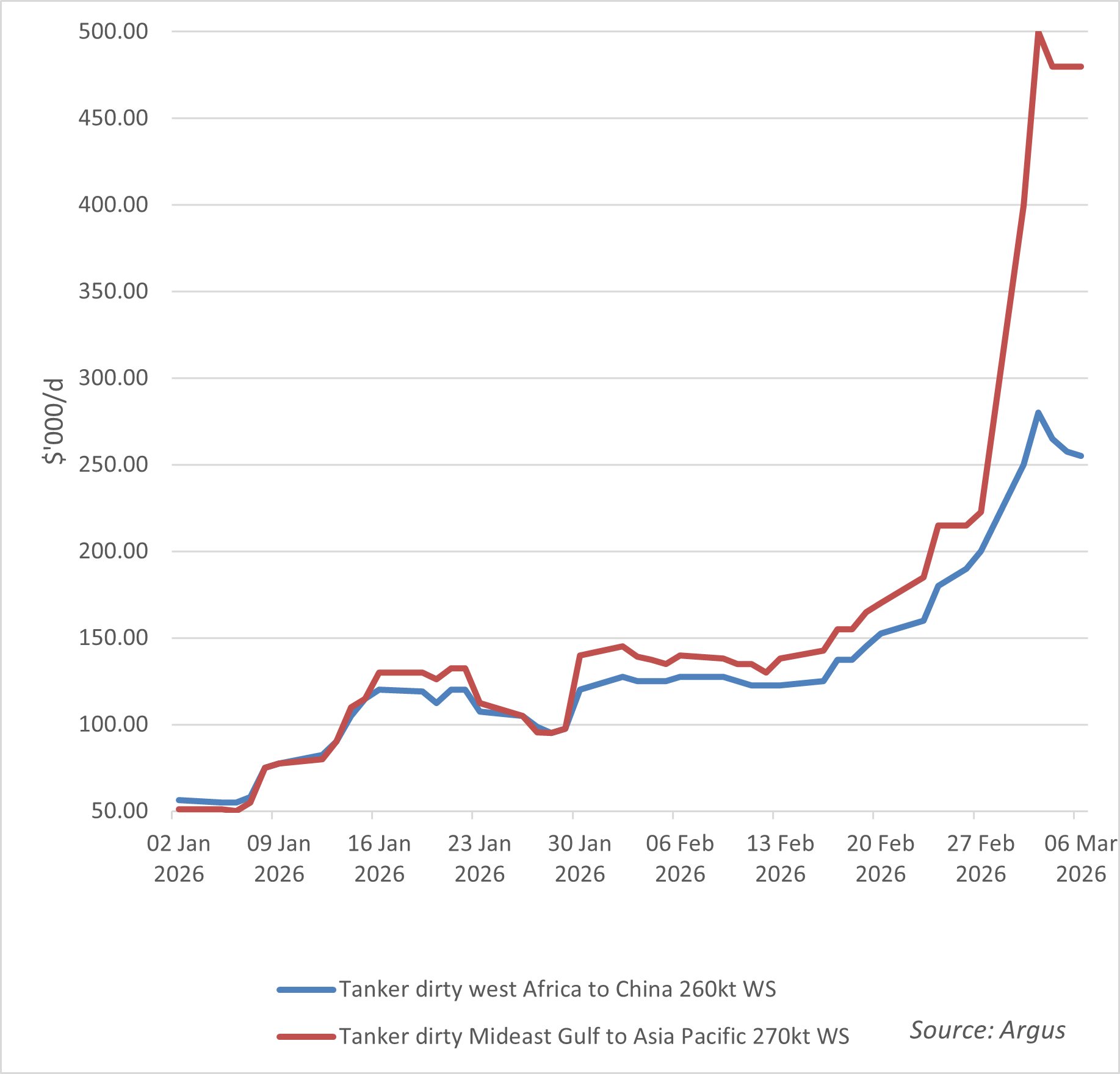

Even this figure understates the true cost to refineries and, by definition, end-users. A crude oil price that impacts the consumer is the one delivered to refinery gates, and freight rates have exploded.

Shipping costs have increased more than fivefold in a matter of days (see Fig.3). A refinery loading a very large crude carrier (VLCC) in Oman may now face transport costs rising from less than $1/bl to as much as $8/bl.

In other words, the delivered cost of Middle Eastern crude to Asian refiners has risen far beyond what futures markets alone would suggest.

Asia will feel the impact first

The burden of these higher costs will fall overwhelmingly on Asia, which imports roughly 90% of Gulf crude exports. Europe and the US each account for less than 5%.

This regional imbalance is already visible in benchmark pricing. Dated Brent is trading below $105/bl—far below the effective price of crude deliverable into the Dubai pricing basket.

The limited barrels still moving out of the region include grades such as Oman, some Murban and Upper Zakum loading via Fujairah, along with Saudi crude increasingly shipped through Yanbu in the Red Sea.

The widening gap between Atlantic Basin and Middle Eastern pricing also reflects structural factors such as inventory levels, government policy and differences in demand elasticity. Developing economies tend to exhibit lower price elasticity of demand: consumption falls less when prices rise.

Shortages emerge first in products

When physical supply is constrained, the first signs appear in petroleum product markets. That pattern is already emerging.

Prices for diesel, jet fuel and fuel oil have surged. Fuel oil is trading above $150/bl, diesel prices have roughly doubled, and jet fuel has reached around $175/bl.

According to the IEA, the global market may face a shortfall of roughly 8m b/d in March. That gap will ultimately be closed through demand destruction—fewer miles driven and fewer flights made.

In practice, much of this adjustment will occur in poorer economies that cannot compete with wealthier countries in bidding for scarce fuel supplies.

The real risk: Policy panic

The simplest solution to the current crisis would be a rapid end to the conflict. But political responses often compound market disruptions.

Governments may resort to export bans, fuel subsidies or price controls in an attempt to shield domestic consumers from rising prices. If adopted widely, such measures would further distort markets and could easily trigger petrol station queues, fuel shortages and even rationing. This would amplify the perception of shortage and cause panic.

Such outcome is unnecessary. Global petroleum inventories remain sufficient to cushion a disruption lasting several weeks.

The challenge is therefore not one of physical scarcity alone, but of policy discipline as well. If governments resist the temptation to interfere excessively in markets, the system can absorb even a severe but temporary disruption.

For now, the oil market does not appear to be panicking. The real question is whether policymakers will remain equally calm.

Adi Imsirovic is a director of consultancy Surrey Clean Energy and a senior associate (non-resident) at CSIS. He is the author of Trading and Price Discovery for Crude Oils: Growth and Development of International Oil Markets, published by Palgrave in 2021, and edited Brent Crude Oil: Genesis and Development of the World’s Most Important Oil Benchmark, published in June 2023. His forthcoming book, The Rivers of Money: A Social and Economic History of Modern Oil Trading, co-written with Colin Bryce, will be published in July this year by Palgrave.

Comments