With a growing population and a drive to increase living standards and combat air pollution, Southeast Asia will need to balance surging energy needs with long-term emissions-reduction commitments.

Natural gas will not only support rising power demand but also help displace more polluting fuels and support the integration of intermittent renewables into the power mix. As such, the region presents long-term macro tailwinds and key market development opportunities for gas and LNG. The challenge lies in improving access to natural gas, a goal now made more difficult following the price volatility driven by the Russia-Ukraine conflict. This will require accelerated development of countries’ own gas reserves and LNG imports at affordable prices.

Due to data availability and stage of gas market development, ‘Southeast Asia’ in this article refers to Indonesia, Malaysia, Thailand, Singapore, Vietnam, the Philippines, Myanmar and Brunei unless mentioned otherwise.

Raising domestic production

Despite the more prominent discourse towards increasing LNG imports, we believe increasing domestic production is an equal pillar in promoting natural gas use in Southeast Asia.

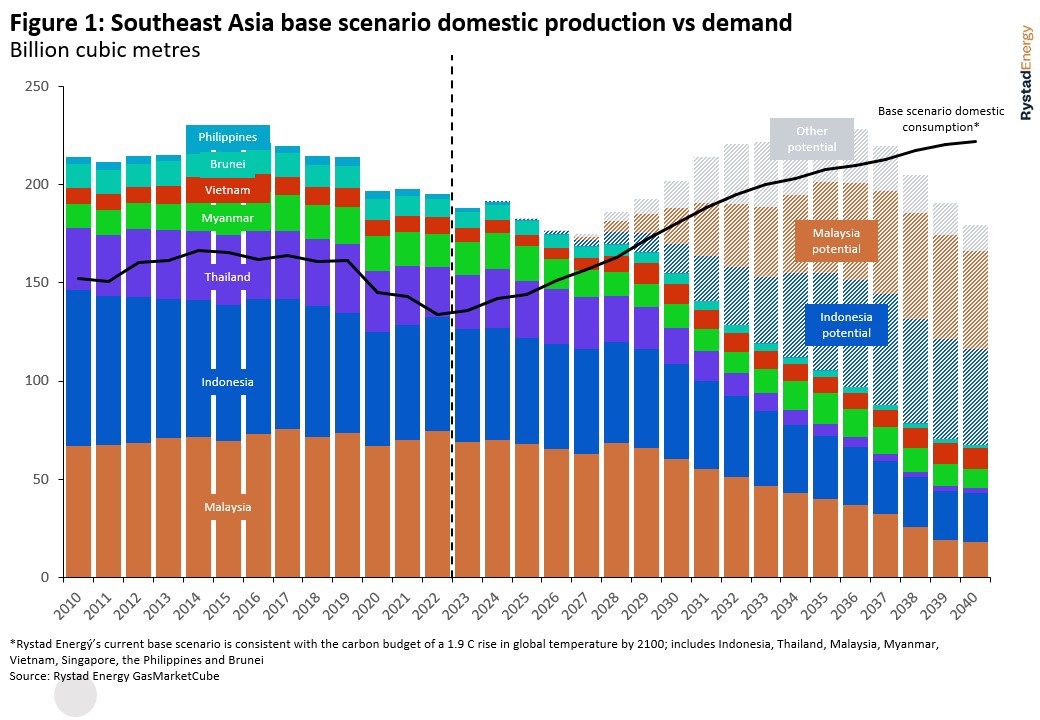

The region continues to hold significant natural gas reserves, with around 85tcf of 2P reserves as of 2022. As shown in , Southeast Asian gas production (including LNG feedgas) peaked in 2016 at around 221bcm, with 2022 production at 192bcm. The outlook is less than encouraging, with base-case production dropping to 154bcm in 2030 and 66bcm in 2040, with downside risk from sanctioning or startup delays. In the same timeframe, Southeast Asian demand (not including LNG feedgas) will increase towards 180bcm by 2030 and 224bcm by 2040. This divergent dynamic is set to turn the region into a net natural gas importer in coming years. However, the timely development of potential resources, including Abadi, Gendalo and Gehem in Indonesia; B14, F38, K5, Kuang North and Kamunsu East in Malaysia; and Ken Bau in Vietnam could help delay regional net imports to after 2035.

With short-term LNG prices having become volatile due to the Russia-Ukraine crisis and long-term LNG prices elevated by structural labour shortages, persistent EPC inflation and, lately, the rising interest rate environment, increasing domestic gas production in Southeast Asia offers an important pathway for the fuel to play a role in the region’s energy transition. The long-term dynamic of increasing demand and declining production means LNG is set to become the marginal source of supply into Southeast Asia, and therefore higher long-term LNG prices may signal new commercial momentum for undeveloped or stalled gas fields.

Pricing is one of many impediments to upstream development in the region, where the prevailing narrative has included convoluted domestic pricing regulations (in Indonesia), regulatory uncertainty, conflicting stakeholder incentives, extensive bureaucracy and divestment by international majors—all of which complicate production in the largely mature region. However, offshore eastern Malaysia presents a significant exception to this narrative, with continued healthy levels of sanctioning and exploration in recent times, as seen by the FID of Rosmari-Marjoram in 2022 and the robust international participation in the Malaysia Bid Round 2022. In addition to supporting domestic consumption in Sabah and Sarawak, these resources can backfill Malaysia LNG, which in turn can support growing regional LNG demand. Similarly, Eni’s acquisition of Chevron’s stakes in the Indonesia Deepwater Development (in addition to its acquisition of Neptune Energy), may also provide optimism for higher production from Bontang.

Despite requiring rapid and unprecedented policy reform, we anticipate accelerated domestic production (where possible) to support burgeoning demand may also be more politically palatable than runaway LNG imports, which may be perceived as promoting import dependence. Furthermore, over the long term (not considering abatement through CCUS), emissions accounting may point to a preference for regionalised trade through pipeline networks or regional LNG trade over large-scale ex-region imports.

Enabling LNG access

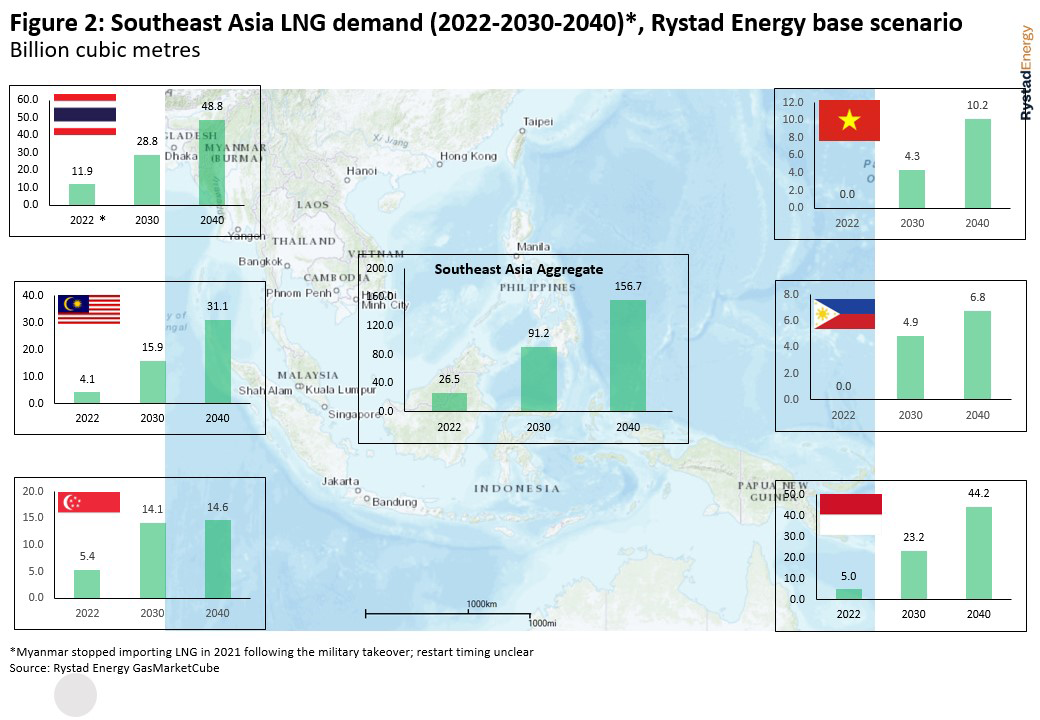

Rising LNG demand (and therefore, exposure to international markets) has been a consequence of declining production and rising gas demand. Since Thailand commenced imports in 2011, the region’s LNG consumption has grown to 26.5bcm as of 2022. Under our base-case scenario for domestic production, LNG demand will grow to 91bcm in 2030 and further to 157bcm by 2040 (Fig. 2), with robust growth in almost every country, including from new importers Vietnam and the Philippines, both of which have an ambitious LNG-to-power pipeline of more than 25GW combined by 2030. For the reasons elaborated later in this article, we remain conservative on how much of this will be achieved.

Affordability remains the largest constraint to LNG imports in Southeast Asia, particularly for emerging importers. Global LNG prices have moderated from the heights of 2022 but, as of August 2023, remain materially higher than pre-crisis averages. Moreover, structural labour shortages and rampant EPC inflation have limited downside movements to long-term prices required to trigger additional LNG production from new projects. In the absence of higher domestic production, the region will be forced to increase LNG imports.

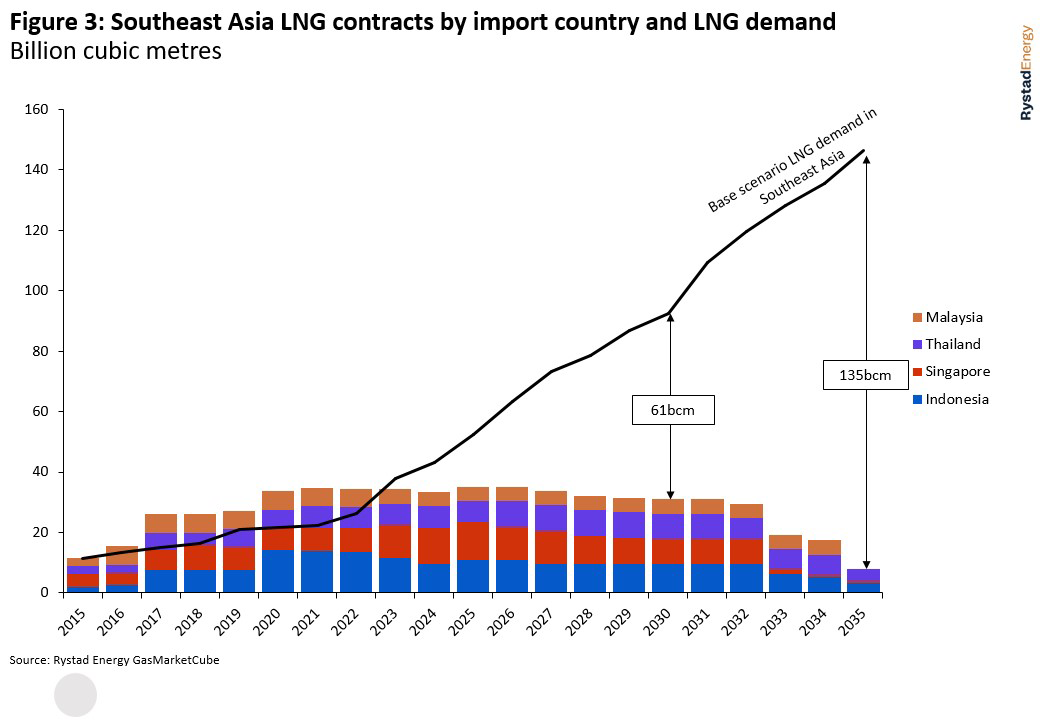

Long-term contracts can provide much-needed price stability and volume certainty required to realise additional import demand. As shown in Fig. 3, Southeast Asian importers had around 35bcm in term contracts (including intra-country contracts as observed in Indonesia), against 26bcm of demand (meaning some of the contract volume was likely diverted to other markets). Rising LNG demand will push the uncontracted quantity to 61bcm by 2030 and 135bcm by 2035. Southeast Asian importers will be keen to close the gap over the next few years, while many majors and portfolio players hold long positions in the second half of the decade after signing on for US LNG offtake and will need to find a market for at least some of these volumes.

In terms of price indexation, it is possible Henry Hub linkage may be welcomed due to the perception of relative stability of US gas prices, especially for LNG-to-power applications where the power-purchase agreements may have fixed cost components, though oil-linkage may also find favour due to precedence. However, the tightening interest rate environment and the strengthening US dollar over the past year may have impacted the credit quality of certain offtakers, making it more challenging for them to sign long-term contracts, leaving them exposed to the spot market and possibly discouraging LNG use. In these cases, government-to-government arrangements could help facilitate more LNG imports.

It is noteworthy that Malaysia and Thailand have embarked on enabling third-party access to their LNG terminals, which will enable competition in their domestic markets and provide clear price signals for new gas investments.

Power and industrial demand

Southeast Asia presents multiple long-term macro tailwinds in support of natural gas demand growth. The region is set to gain substantial economic prominence, with real GDP expected to more than double in 2050 from $3.6t in 2022, in conjunction with population growth of over 100m in the same timeframe. Higher urbanisation will also drive more electricity demand through space cooling requirements.

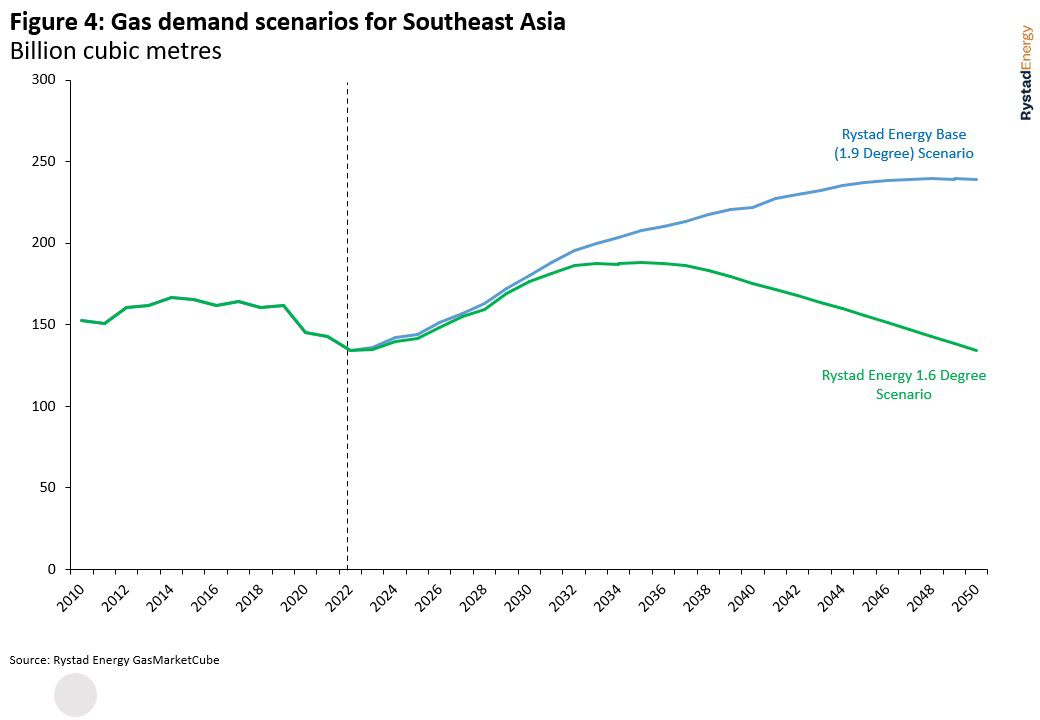

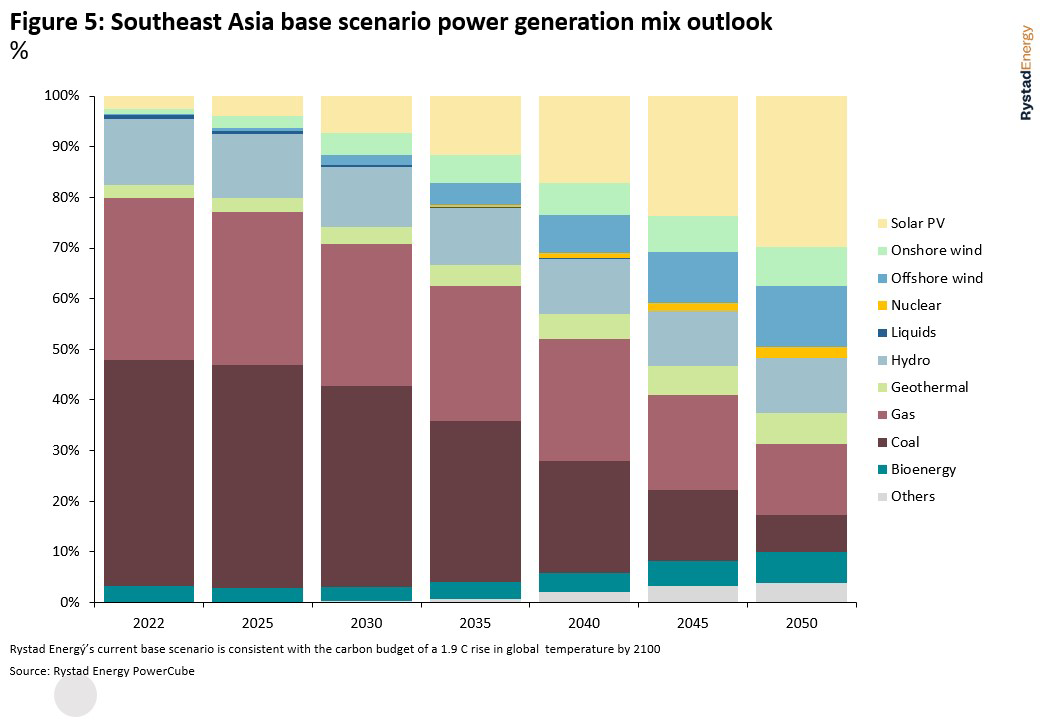

As per Fig. 4, in our base (1.9°C) scenario, Southeast Asian natural gas consumption is set to grow continuously until it peaks in the late 2040s at around 247bcm. Demand in the power sector is set to grow until around 2037, while demand in the industrial sector can continue to grow into the 2040s due to limited availability of substitutes for process heat and feedstock. Note that further upside from the power sector is possible through more policy support for coal-to-gas switching (such as a carbon price) or lower gas prices. Common drivers across countries include rising power demand, ambitious renewables generation targets and coal phasedowns. Some industrial sector demand growth is expected in Indonesia, Malaysia and Thailand due to petrochemical or gas processing plant capacity additions. Furthermore, Thailand is the only Southeast Asian country where gas use in the transport sector has caught hold, although this may eventually be phased down in favour of electric vehicles.

Even in our accelerated energy transition scenario, which corresponds to a 1.6°C change in temperature by 2100, demand continues to grow along a nearly identical pathway as our base scenario until after 2030 and peaks around 2035 at 188bcm before declining to 134bcm by 2050.

The difference is driven by lower gas consumption in the power sector in the 1.6°C scenario: it is important to ensure gas access to facilitate the power sector’s transition away from coal and towards more renewables so that electricity can then be used to decarbonise the industrial, building and transportation sectors.

It is also worth noting that much of Southeast Asia is already gasified, with natural gas making up some 20% of the primary energy mix and some 32% of the power mix (2022), with substantial existing or planned infrastructure. The region therefore poses relatively less adoption risk for natural gas and infrastructure challenges than others where gas use is unfamiliar.

Key risks to gas’ future in Southeast Asia

The role of natural gas in Southeast Asia’s power sector has been complicated by incumbent coal and competitive and emissions-free renewables. The supply uncertainty posed by the dynamic of declining domestic production and high international LNG prices means coal may continue to find favour in the power mix over the medium term. Given Indonesia and Vietnam are major coal producers, the fuel is still seen as affordable and reliable, and due to energy security concerns may take precedence over natural gas in the absence of more policy support, even as the need to phase down coal is widely acknowledged.

The region has also made tremendous strides towards renewables capacity additions and net-zero targets in recent years (nine out of ten governments have net-zero targets, the latest by 2065). Even as gas is a complement to renewables in coal-heavy grids, the long-term trend of declining renewable generation costs means LNG may not be able to compete on baseload, which is what is required to guarantee long-term offtake from import terminals. Between 2015 and 2022, Vietnam added 18GW of solar and about 4GW of wind capacity, which by 2030 will grow to 25GW and 29GW respectively. We also anticipate similarly robust growth in the Philippines, with nearly 30GW of solar and 9GW of wind capacity by 2030. Other countries in the region will also have smaller renewables capacity additions, while Singapore has turned to importing 100MW of hydroelectricity from Laos.

High international LNG prices coupled with the impact of domestic currency deterioration mean that it is also unclear which suppliers would accept direct long-term exposure to the credit profiles of emerging LNG buyers in the absence of back-to-back power-purchase agreements guaranteeing revenue along the chain—and supplying to them would likely need intermediary traders or portfolio players with a higher risk tolerance or government-to-government agreements. The archipelago geography of the region also means some demand will have to be met through small-scale supply chains, which accordingly increases cost (and risk) for project sponsors.

Gas still a solution

Like other emerging regions around the world, the burgeoning energy needs of Southeast Asia make it unlikely that renewables alone will meet energy demand growth out to 2050. Therefore, gas retains an important and sustained role in balancing the transition of the power sector.

This article paints a broad picture of the role of natural gas in Southeast Asia, but the reality is that economic development and stage of energy transition vary by country, and therefore individual pathways to economic prosperity and decarbonisation could vary significantly. Meeting the demand potential derived from macro tailwinds depends on material policy reform and regulatory certainty to increase domestic production and affordability to increase LNG imports—all of which are challenging to pull off. Even as its credentials in the energy transition may be questioned in other parts of the world, Southeast Asia is an area where the high degree of coal dependence, and indeed continuing coal capacity construction, means natural gas is still a solution.

Kaushal Ramesh is vice-president, head of gas & LNG analytics at Rystad Energy. Jun Yee Chew is vice-president and head of APAC renewables & power markets research at Rystad Energy. Prateek Pandey is vice-president of upstream research at Rystad Energy. Visit Rystad Energy at www.rystadenergy.com.

This article is part of our special LNG's role in resolving Asia's trilemma report, which looks at what the energy crisis means for LNG and what LNG's role is in resolving Asia's trilemma. Click here to download the full report, or visit the Gulf Energy Information stand (E326) at Gastech 2023 to pick up a copy.

Comments