The Americas have undergone a profound energy transformation, evolving from a marginal energy player to the world’s most crucial and dynamic source of LNG.

This energy revolution, catalysed by the sheer scale of North American gas reserves, is now entering its second, more complex phase: a global construction race, backed by an unprecedented mix of corporate and international capital. For a world demanding cleaner, more flexible and geographically diverse energy, the vast 278mt/yr pipeline of new capacity in the Americas represents the definitive future of the global LNG market.

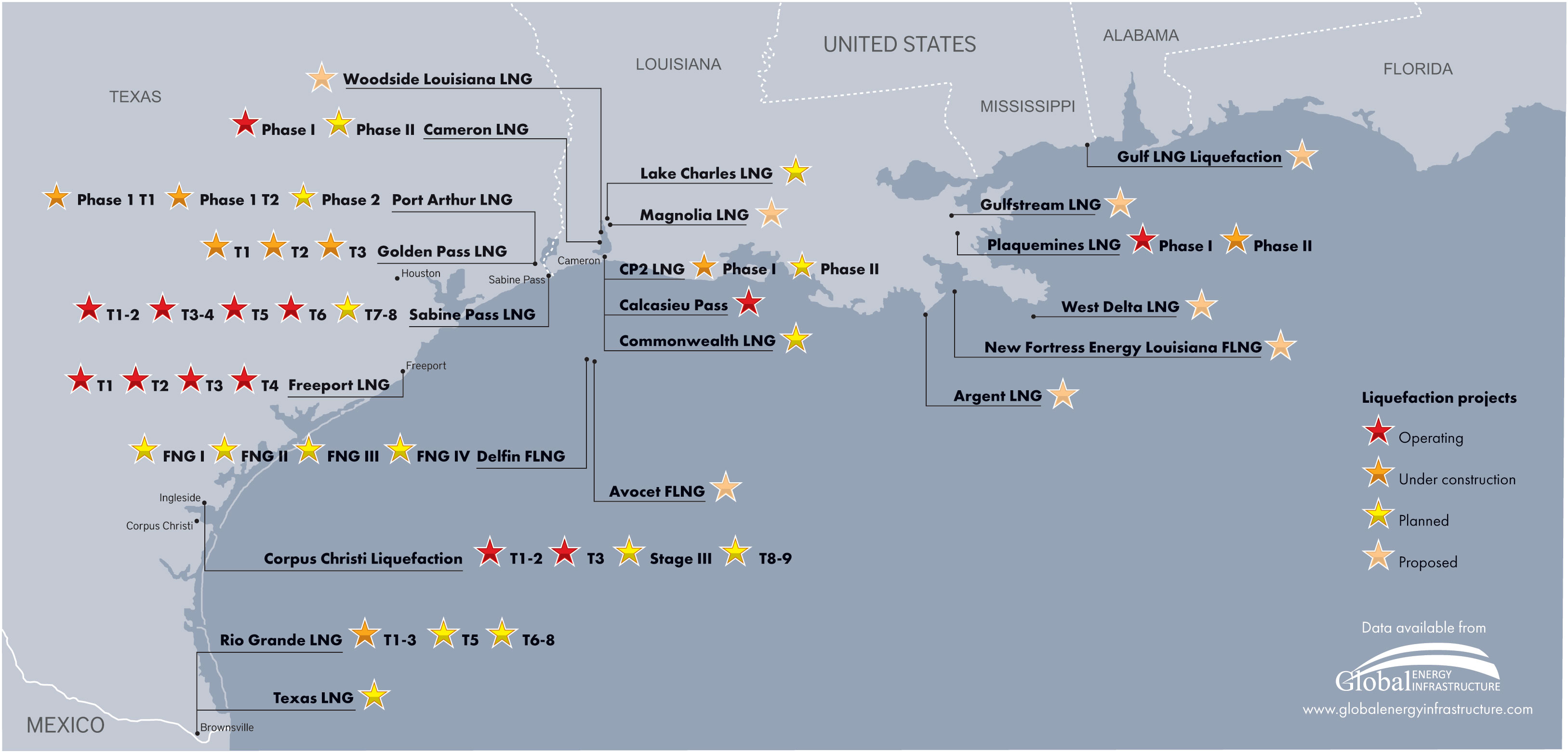

North American export expansion continues

Information from Global Energy Infrastructure (GEI) confirms the Americas are structured as a primary exporter to the global market. The continent’s combined operating liquefaction capacity stands at 141.93mt/yr, an already formidable figure that is being rapidly superseded by a staggering 85.73mt/yr currently under construction. This wave of expansion, particularly centred in the Gulf Coast of the US, is cementing the continent's role as the central pillar of global supply.

The US remains the undisputed anchor of this growth, currently boasting 105.88mt/yr of operating export capacity, making it the largest liquefier globally, and is leading the next expansion wave with an additional 75.68mt/yr under construction.

While the US dominates the numbers, the regional expansion is diverse:

- Canada is making a strategic push, with 14mt/yr operating and a further 5.4mt/yr under construction, offering key access to Pacific markets.

- Trinidad and Tobago, a long-established Caribbean player, maintains a substantial base of 14.8mt/yr operating capacity (although the Atlantic LNG facility has been operating below its full capacity for several years due to a shortfall in natural gas supply).

- Mexico is emerging as a critical transit hub. While historically an importer, it is leveraging its proximity to US gas, with 4.65mt/yr of export capacity under construction (in addition to 2.8mt/yr already operating) focused on re-exporting gas from terminals on both its Pacific and Gulf coasts.

This massive commitment to new liquefaction capacity, with a further 185.45mt/yr in the planned or potential stages, underscores a long-term economic and geopolitical conviction that the Americas gas supply has potential to power the world's energy transition for decades to come.

The scale of this expansion requires enormous capital, engineering expertise and risk management, which has led to a highly concentrated group of operators and a complex web of international shareholders shaping the future market.

Mega-projects now require syndicated financing, bringing together NOCs, sovereign wealth funds and private capital. The Rio Grande project (the first three trains of which are under construction with 17.61mt/yr), led by NextDecade , epitomises this trend, featuring a global consortium of shareholders including infrastructure investor Global Infrastructure Partners, Singaporean sovereign wealth fund GIC, TotalEnergies, the UAE’s ADNOC and state-owned investment company Mubadala. This mix of Asian and Middle Eastern capital highlights the global appetite for owning a piece of the American supply chain.

Major players are combining their technical prowess with strategic external financing to de-risk projects and secure essential long-term buyers. ExxonMobil, for example, is constructing a significant 18mt/yr of future capacity in partnership with state-owned QatarEnergy, which holds a 70% stake in the Golden Pass LNG phases. This partnership is a powerful signal of cross-regional cooperation.

Similarly, Sempra is an infrastructure firm with an LNG portfolio in the US and Mexico totalling 27.5mt/yr in future capacity, secured by a dense network of partners. These alliances include private equity firm KKR, superindie ConocoPhillips, TotalEnergies and influential Japanese trading houses such as Mitsui Group and Mitsubishi Corporation. The involvement of these international buyers and investors is crucial for guaranteeing long-term offtake volumes.

A few companies are making large commitments with high internal equity. Venture Global LNG is maintaining 100% ownership of its 16.67mt/yr of capacity being constructed at the CP2 LNG and Plaquemines LNG projects, demonstrating confidence in its execution and commercial strategy. In contrast, the 20.1mt/yr capacity advanced by the Alaska Gasline Development Corp in partnership with Glenfarne showcases the continued, yet complex, role of state-aligned entities in unlocking new resource basins.

These figures underscore the scale of the financial commitment required. Operators such as Argent LNG (20.0mt/yr proposed) and Woodside Energy (16.5mt/yr proposed) are making massive, long-term bets that will determine the future of global energy flows.

FIG.1: LIQUEFACTION CAPACITY BY STATUS ACROSS THE AMERICAS

| Country | Operating, mt/yr | Under construction**, mt/yr | Planned or potential†, mt/yr | Total, mt/yr |

| 28.7 | ||||

| Peru | – | |||

| 4.65 | ||||

| – | ||||

South America’s import security challenge

While the North is focused on exporting, the South remains critically dependent on LNG imports to fuel its grid and industry. The region operates with a robust 174.18mt/yr of regasification capacity, exceeding current export capacity and highlighting the continent's energy duality.

Brazil stands out as the largest South American regasifier, with 41.64mt/yr of capacity. Brazil's reliance on LNG is directly tied to the need for thermal power generation to back up its vast, but weather-dependent, hydroelectric system. Similarly, Argentina (with 7mt/yr of operating capacity) and Chile (with 5.25mt/yr) use LNG as a critical energy buffer, often utilising FSRUs for flexible access to gas.

Though smaller in scale than the export side, the 4.7mt/yr of import capacity under construction across the region confirms the continued commitment to energy security and flexible gas access, particularly in countries such as Brazil and Honduras.

Americas securing long-term energy supply

The massive, decade-long build-out of LNG capacity across the Americas is not merely a boom cycle; it is a structural market transformation. With hundreds of millions of tonnes of new capacity slated to come online between 2025 and 2033, the continent is fundamentally rewriting the global energy supply map.

The GEI data confirms that the future LNG market will be defined by scale, resilience and complex risk management. The sheer volume of committed capacity, backed by a diverse consortium of operators, ensures the Americas will be the essential engine for global gas supply growth.

For international buyers, this pipeline offers unprecedented supply chain security and optionality, providing a reliable counterweight to traditional, less flexible sources. For the operators, however, the challenge shifts from securing financing to managing the future supply glut. Successfully navigating the next decade will require shrewd commercial strategies to lock in long-term contracts amidst heightened competition.

Ultimately, the commitment of capital and resources to LNG in the Americas is a decisive investment in a long-term future powered by gas. It is a defining moment for the continent, establishing it as the indispensable heart of a more stable, yet fiercely competitive, global energy market.

Peregrine Bush is senior director, data and technology, at Global Energy Infrastructure. This article is taken from our Outlook 2026 report. To read Outlook 2026 in full, click here.

Comments