Outlook 2024: Building LNG’s resilience through turbulent times

Larger and more diversified portfolios are best placed to navigate through volatility

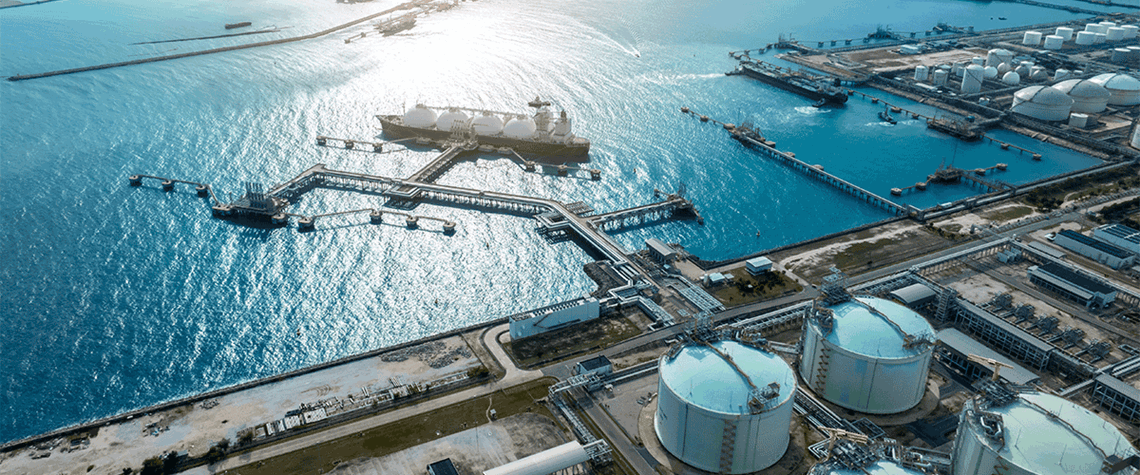

The global LNG industry is thriving. A record 200mt/yr of new supply is under construction as players bet big on Asia’s push to reduce its dependence on coal and Europe’s need to replace Russian gas. Given the urgency of the energy transition, an increasingly fractious geopolitical system and concerns over global economic growth, could the LNG industry have bitten off more than it can chew? In this article, we explore some of the market and external risks that players need to grapple with and consider how they can prosper through turbulent times. Is there too much LNG under construction? In short, no. Increased supply availability will bring prices down and boost demand growth. In our latest

Also in this section

2 April 2026

Alongside a rapid continued build-out of renewables, China’s latest five-year plan stresses the value of domestic hydrocarbon production for energy security and calls for increased Russian gas imports

2 April 2026

The government is taking important steps to revive domestic production, lift investment and benefit from the geopolitical crisis even if more needs to be done in the longer term

1 April 2026

Golden Pass’s startup offers QatarEnergy a timely boost but may also force a difficult choice between honouring disrupted contracts and capitalising on soaring spot LNG prices

1 April 2026

It is not a case of if or when, but the length and magnitude of economic damage from elevated oil prices