In 2023, Vietnam and the Philippines both opened their first LNG import terminals, both LNG-to-power projects. The entry of Vietnam and the Philippines into LNG markets heralds a new era for the fuel in the region. The project pipeline for Southeast Asia will see 24m t/y of new LNG import capacity added before 2030, an increase of 45%.

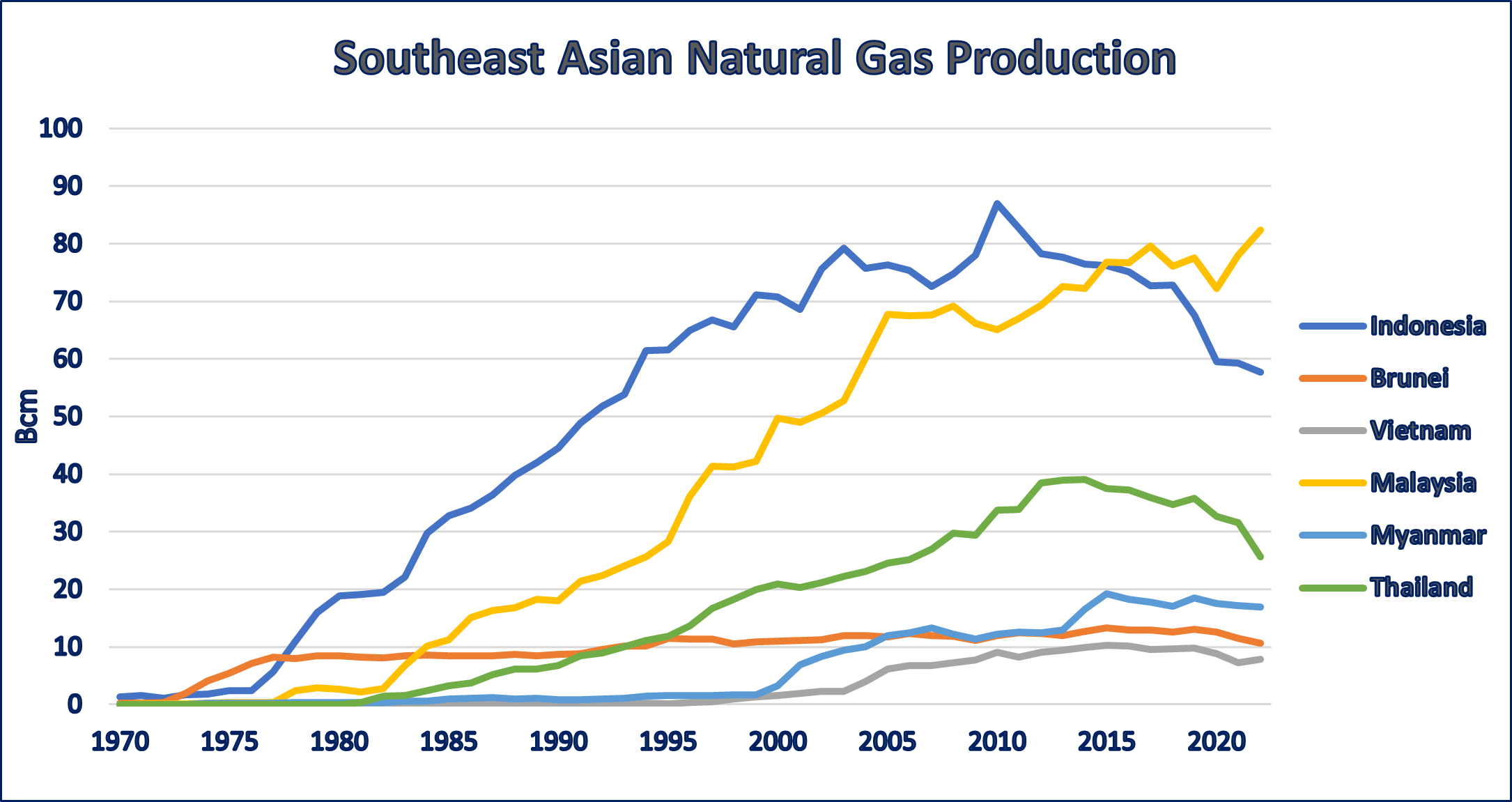

The backdrop to this expansion is fast-growing economies and declining natural gas production. Southeast Asia is endowed with substantial natural gas resources with few outlets for export beyond the region. As a result, since the 1970s and 1980s when production began climbing, natural gas has played an important role in the region’s energy mix. This is particularly true for electricity generation, with gas’s share electric generation peaking as high as 75% in Thailand in 2010. However, since c.2010, gas production has stagnated or begun declining across most of the region.

Meanwhile, Southeast Asia’s economies continue to grow quickly. The region is expected to see GDP growth between 4% and 5% over the next few years. Economic growth is driving electricity demand up even as domestic gas has production has stagnated or declined.

In response, countries in the region have seen coal’s share of power generation expand. Vietnam saw its share of coal in power generation rise from 17% in 2010 to 49% in 2020, as gas’ share declined from 48% to 11%. And in the Philippines, coal’s share grew from 31% in 2010 to 47% in 2022, as gas’s share fell from 19% to 12.5%.

But as climate change looms larger, many countries are looking to limit coal use in line with decarbonisation objectives. Renewables are expected to play a role in displacing coal, but many countries are also looking to gas again. In addition to burning cleaner than coal, gas is also attractive as projects tend to have smaller capital costs and are perceived as faster and easier to build. This turn back to gas is driving the growth in LNG projects across the region as a supplement to domestic gas.

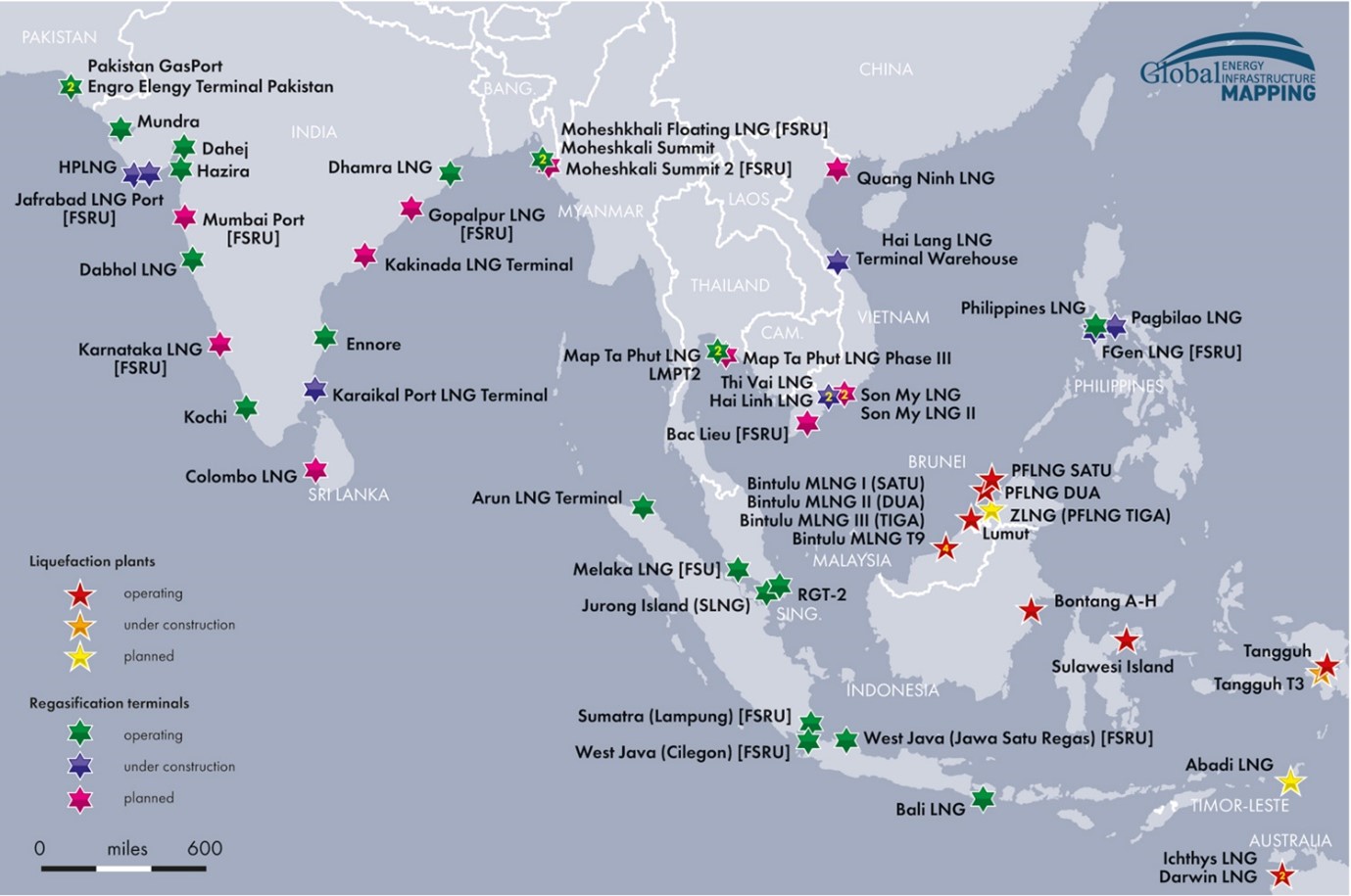

Prior to 2023, Southeast Asian LNG infrastructure was largely concentrated in Thailand, Malaysia, and Indonesia, which are also the region’s largest gas producers. Indonesia and Malaysia have invested in significant LNG liquefaction capacity, and along with the tiny Sultanate of Brunei, they have 70m t/y of liquefaction capacity, or about 15% of global capacity.

Malaysia and Indonesia also have most of Southeast Asia’s regasification capacity. The countries’ domestic gas resources are separated from demand centres by ocean. Liquefaction and regasification terminals in the countries not only participate in international trade but allow natural gas to be moved from fields on Borneo, Sulawesi, and New Guinea to cities on the Malay Peninsula and Java, as well to smaller islands which lack pipeline connections to gas networks.

While in Malaysia, gas production has continued to rise, in Indonesia LNG exports have fallen precipitously over the last decade as gas production shrinks and exports are increasingly crowded out by domestic demand. Although a major LNG terminal expansion, Tangguh LNG T3, is scheduled to open in 2023, Indonesian government officials have openly discussed prioritising domestic energy security by banning future LNG exports once existing contracts expire.

Southeast Asia’s third biggest gas producer, Thailand, has eschewed exports. The country has substantial domestic gas resources, production peaked at 39bcm/y in 2014 and it continues to produce c.25bcm/y of gas. But this production is kept in the country where it feeds electricity generation. Out of all Southeast Asian nations, only Malaysia is as dependent on gas as Thailand is. As a share of primary energy consumption, gas peaked at close to 40% in Thailand and still makes up 32% of energy consumption.

Despite its relatively high gas production, Thailand imports gas from neighbouring Myanmar and has increasingly leaned on LNG imports as gas production has declined further. While domestic gas continues to cover c.80% of Thailand’s consumption, LNG imports rose from 1m t/y in 2011 to 11m t/y in 2022. To support rising imports, a second LNG terminal in Ma Ta Phut was opened in 2022, and an expansion to the older Ma Ta Phut terminal is planned. Import capacity could reach 19m t/y by the end of 2027.

But while Thailand’s attachment to gas means LNG can play an important role in substituting for falling domestic production, gas has little role to play in decarbonisation. Gas’ share of the electricity mix is already high, and Thailand has little room to replace coal with gas. Instead, in its most recent Power Development Plans (revised in 2020), Thailand communicated its intention to diversify away from gas to reduce its vulnerability to shortages. The plan would see aggressive cuts in natural gas’s share of electricity generation, from c.60% when adopted to 37% in 2036, with the change driven by a big increase in hydropower and renewable’s share of generation, in addition to a small increase in coal’s share of generation. Thailand is unlikely to see much new LNG infrastructure as a result. Its Power Development Plan mentions the fuel only twice, both times in passing.

Singapore is a final incumbent importer of LNG in Southeast Asia. An LNG terminal opened in 2013 has helped the country to diversify its gas supply away from Malaysian pipeline imports. A project that is vital to the city state’s energy security as more than 90% of its electricity is generated using gas. The Jurong Island LNG terminal imports enough gas to supply c.40% of the Singapore’s gas and still operates significantly under capacity.

The new markets of Vietnam and the Philippines will be the site of most growth in LNG import capacity. Across 10 projects, the countries will add 22m t/y of capacity between now and 2027, with the two terminals already opened in 2023 representing an additional 6m t/yr. Vietnam and the Philippines rely on gas less than the region’s other LNG importers, the fuel makes up 5% and 6% of their primary energy consumption respectively.

For Vietnam, in addition to being a cleaner alternative to coal, LNG is seen as a way to diversify the country’s electricity supply away from hydropower and reduce vulnerability to drought. In Power Development Plan VIII, formally adopted in May, Vietnam presented its intention to substantially increase gas’s share in electricity generation from 10% in 2022 to 25% in 2030.

Although the plan also envisages turning around Vietnam’s falling gas production, the increase in gas use is largely expected to come on the back of LNG imports, with LNG-to-power plants providing 60% of all gas-fired electricity. Up from zero when the plan was adopted. Supporting these new LNG-fired power plants will be new LNG terminals. In addition to the already completed Thi Vai terminal, and its expansion expected next year, six LNG terminals are in active development, representing c.16m t/y of additional LNG import capacity. More terminals are expected to serve all [14] LNG-to-power plants listed in Vietnam’s Power Development Plan VIII.

In the Philippines, the project pipeline is smaller, but LNG-to-power is still set to play a big role in the country’s energy mix. The Philippines has in the past consumed less gas than other nations in the region, in large part because gas production in the Philippines is so much lower. Production peaked at 4.4mcm in 2019 and then declined steeply. In 2023, gas production is on track to be below 2mcm. AG&P’s new terminal in the Philippines will already more than replace this shortfall.

But the Philippines’ Power Development Plan envisions gas-fired generation capacity increasing almost four-fold by 2035. While the country only has two LNG projects at an advanced stage of development, both expected within the next year, there is room for demand to grow and more projects will likely progress to serve that demand.

New Era Delayed

Despite the important milestones in 2023 for Southeast Asian LNG, the new age of LNG-to-power in Southeast Asia remains a few years off. This is particularly true in Vietnam where besides the already operating Thi Vai LNG, all projects have been pushed back to 2025 or later. Hai Linh LNG, expected to be Vietnam’s first LNG terminal when it was completed in 2020, has yet to receive a cargo and is now expected to begin operations in 2025. Delta Offshore Energy’s Bac Lieu LNG terminal initially was looking to start up in 2023 but is now targeting a 2028 startup date.

LNG projects in the Philippines are more front-loaded, with two more terminals expected by the end of 2023. But beside those projects there is little else expected in the Philippines on the LNG-to-power front until the second half of the decade.

The delay is in some ways advantageous. The period from 2025 to 2027 will see an explosion in global LNG supply as Qatar’s and the United States complete huge capacity additions. Sky-high LNG prices in 2022 showed the risks of depending on the fuel too strongly. Southeast Asian buyers are unlikely to reliably outbid the large European and Northeast Asian buyers in the tight market.

The region’s relationship with LNG remains complicated and uneven as countries transition to gas on one side and transition from gas on the other, but the infrastructure build out is pushing ahead.

This article is part of our special LNG's role in resolving Asia's trilemma report, which looks at what the energy crisis means for LNG and what LNG's role is in resolving Asia's trilemma. Click here to download the full report, or visit the Gulf Energy Information stand (E326) at Gastech 2023 to pick up a copy.

Comments